The energy trilemma in focus: the price of dependence

Europe’s approach to energy policy has been in transition since the 2022 energy crisis laid bare the continent’s dependence on imported fossil fuels. More recently, the outbreak of war in the Middle East and the subsequent disruption to global oil and gas markets have caused further challenges. This article uses the framework of the ‘energy trilemma’—balancing security of supply, affordability, and environmental sustainability—to examine the policy responses taking shape across Europe, and the trade-offs that governments face between protecting consumers and industry in the near term and staying the course on decarbonisation. This article is the second in a series exploring various topics affecting the energy system under this ongoing uncertainty. The first article covered energy market design trends, including interventions in gas markets and the Emissions Trading System (ETS).

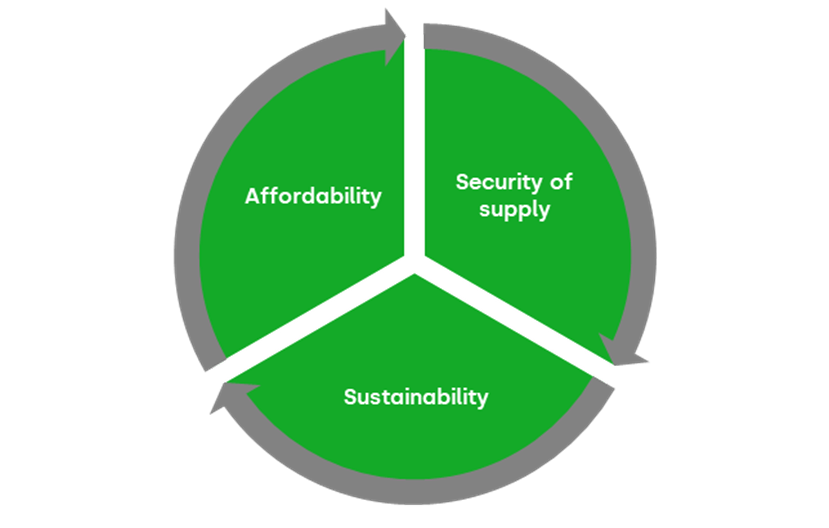

The concept of the ‘energy trilemma’ has been a cornerstone of energy policy debate since the 1990s. Policymakers began using the framework to weigh up three competing interests when setting energy policy, which are illustrated in Figure 1 below.1

Figure 1 The energy trilemma

The three dimensions can be described as follows.

- Security of supply is defined as ‘the availability of energy at all times in various forms, in sufficient quantities, and at reasonable and/or affordable prices.’2

- Affordability refers to the accessibility and fair pricing of energy for households and businesses alike, ensuring that the costs of the system are distributed in a manner that society can sustain.3

- Sustainability concerns the imperative to provide energy services for all people now and in the future in a manner that is sustainable, implying the reduction of carbon intensity of energy systems and honouring the commitments made under the Paris Agreement and successor frameworks.4

The trilemma encapsulates the challenge of balancing these three pivotal objectives simultaneously.

A new shock and the effects on the trilemma

The energy trilemma is particularly relevant against the current geopolitical backdrop. The Strait of Hormuz connecting Iran, the UAE and Oman was closed on 28 February 2026 as part of the Iran war,5 becoming the largest disruption to world energy supply since the oil crises of the 1970s. Following the effective closure, oil and liquified natural gas (LNG) exports became stranded, causing prices to spike.6 The war has precipitated a second major energy crisis and subsequently an economic crisis for Europe, primarily through the suspension of LNG shipments—a supply source that European buyers had actively cultivated as a replacement for Russian pipeline gas after the Russian invasion of Ukraine in 2022.7 Even if the war ends tomorrow, it will take time for supply conditions to revert to pre-war levels.8

In 2025, approximately 20m barrels of oil and oil products passed through the Strait of Hormuz per day, according to estimates from the US Energy Information Administration.9 The strait is the single most important chokepoint in global energy trade—and its disruption does not affect merely the price of a commodity. It strikes simultaneously at all three corners of the trilemma: security of supply is directly affected; affordability deteriorates sharply for households and industry; and the policy bandwidth needed to manage the long-term decarbonisation agenda tends to be consumed by crisis management.

Further considerations within the trilemma? The role of industrial competitiveness

At the same time there are growing discussions around industrial competitiveness as a further objective of energy policy. The risk of carbon leakage,10 the competitive pressure from subsidised clean-technology manufacturing elsewhere, and the risk of deindustrialisation in energy-intensive sectors, have all elevated competitiveness from a side constraint to a structural policy concern.11 The Hormuz shock has intensified that pressure considerably: energy-intensive industries across Europe are facing input cost spikes at the same moment as they are being asked to invest in capital-heavy decarbonisation. Even beyond energy, the oil and gas blockade in the Strait of Hormuz will tighten petrochemical and fertiliser markets, with significant geopolitical and economic consequences.12

In the remainder of this article we explore how governments and regulators manage this balancing act under conditions of acute stress—maintaining strategic focus on long-term decarbonisation objectives while responding to near-term pressures on costs, security of supply and competitiveness. We examine the trade-offs currently being debated across several geographies, considering both the case for doubling down on the transition and the temptation to slow it.

An opportunity to double down?

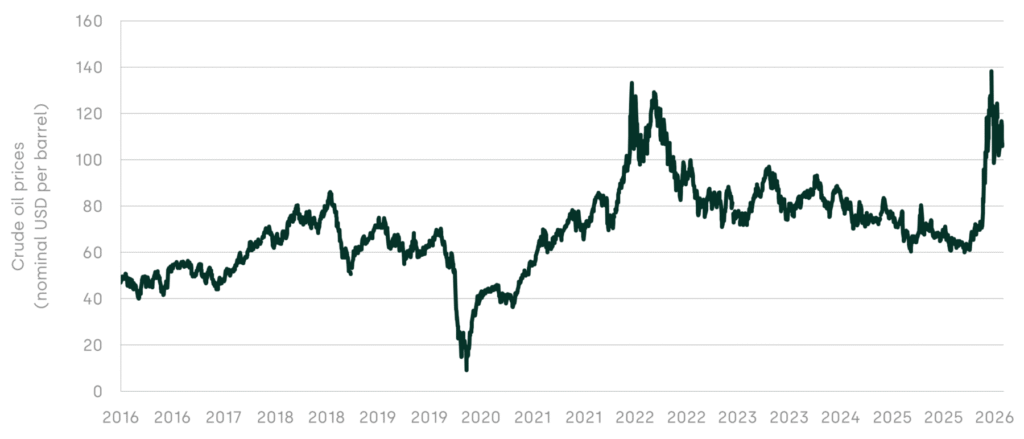

Crises tend to disrupt long time horizons. As shown in Figure 2, the Hormuz closure has led to oil prices spiking to levels not seen since the worst months of the price shock after the start of the war in Ukraine—around double the level seen in the last two years.

Figure 2 Crude oil prices: Brent–Europe

Similarly, LNG prices have surged as the European gas benchmark rose more than 40% in response to the closure of the Strait of Hormuz and remained stable at this elevated level for the following months.13 When wholesale prices spike, the political pressure to protect consumers and industry from the immediate cost becomes intense. Figure 3 shows some of the news headlines in different European countries that are particular concerned about rising oil prices.

Figure 3 Examples of media headlines

The political pressure to address cost increases can override the slower logic of long-run investment signals, as discussed below.

Double down or slow down?

The central energy policy dilemma crystallised by the Hormuz crisis can be framed as a choice between two broad responses. Doubling down means accelerating the energy transition on the grounds that energy independence and renewable energy are two sides of the same coin—this reflects the view that the fastest route away from exposure to volatile global fossil-fuel markets may be through investment in domestic, price-stable, low-carbon sources. Slowing down means prioritising affordability and near-term security of supply by means of extending the life of fossil-fuel assets or deferring investment in new low-carbon infrastructure, in turn prolonging the dependence on fossil fuels and volatile commodity prices.

The President of the European Commission, Ursula von der Leyen, has called for accelerating renewables-led electrification in direct response to the Iran conflict.14 This position has been formalised through the Commission’s AccelerateEU initiative, which explicitly calls for a shift to homegrown clean energy to achieve energy independence and security.15 European governments are poised to call for swifter deployment of clean energy to combat fossil-fuel shocks as the Iran crisis drives up prices.16 The war in Iran has prompted analysts to ask whether this is the ‘electroshock’ needed for the European energy transition.17 The logic is that a crisis rooted in dependence on Middle Eastern fossil-fuel flows is, by definition, a crisis from which domestic renewables, storage, and nuclear power generation can offer strategic protection.

The ongoing policy programmes aimed at accelerating the energy transition are not responses to the current crisis—they represent long-term structural plans that predate it, even if both the current and previous (2022–23 Russia/Ukraine) energy crises have strengthened the political case for them.18 Across European energy systems, a mixed equilibrium is emerging. Specifically, the future energy mix is likely to reflect national circumstances at given points in time rather than a single European approach.19 The pace at which nations can expand renewable generation, develop long-term storage, build out heat networks, and attract the capital needed to underpin industrial decarbonisation varies enormously. This is due to “economic endowment effects”, in other words shaped by geography, grid architecture, institutional capacity and the structure of domestic energy markets.

Denmark is an example of a country that is at the forefront of renewable energy generation. The green transition in Denmark has been driven by sustained investment in research and development (R&D), institutional support for planning and installation of renewable energy sources, and the introduction of feed-in tariffs for wind in the 1980s.20 As Denmark is a flat country bordering the sea, the implementation of off- and onshore wind farms has been relatively easy. Its grid architecture, defined by having one state-owned transmission system operator (TSO) and open access to distribution system operators (DSOs), strong grid interconnection, and constant upgrading of aging renewable infrastructure have further enabled Denmark’s green transition.21

Poland, instead, is an example of a country that still produces over half of its electricity from coal and has been slow in delivering key legislation amid political turmoil.22

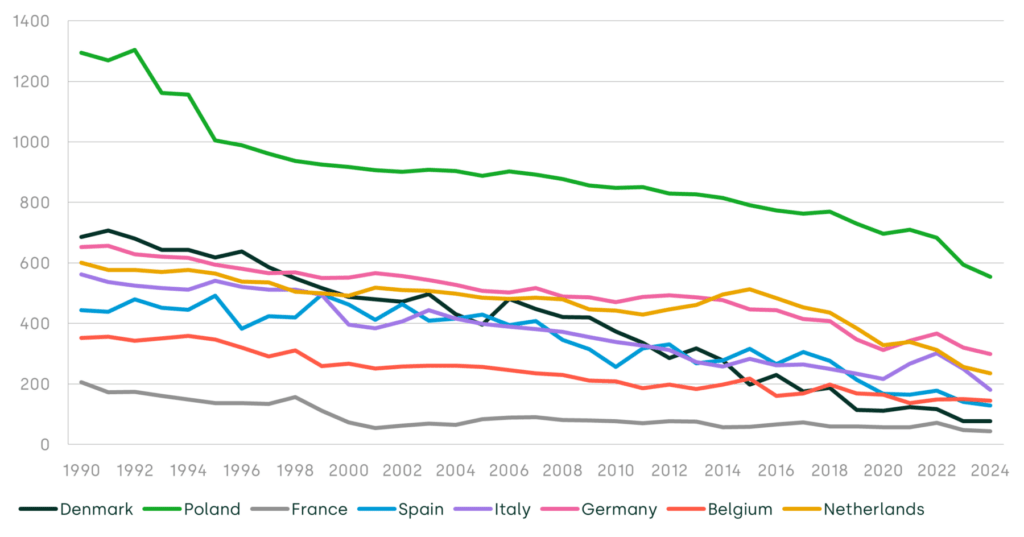

As Figure 4 below illustrates, the carbon intensity of electricity generation has fallen substantially across different European countries over the past three decades, but the starting points and rates of progress differ markedly by country.

Figure 4 Greenhouse gas emission intensity of electricity generation in selected countries over 1990–2024 (gCO2e/kWh)

This divergence matters for the policy choices that each country faces today: a country that has already decarbonised much of its grid does not need to rely on gas- or coal-fired plants, and would face different trade-offs when reacting to a supply shock of this magnitude, relative to a country that is at an earlier stage of the energy transition.

It seems that a blended equilibrium is already taking shape across European energy systems, where the future energy mix will mirror individual national circumstances rather than follow a single, unified European approach. This is evident in the following areas.

- Renewables, storage and nuclear. Most European countries are accelerating renewable capacity commitments in direct response to the shock. France’s nuclear strategy—already central to its long-term energy planning—has been reinforced by the crisis, as the price stability of nuclear generation stands in sharp contrast to the volatility of gas-generated power.23 Other countries are focusing on expanding grid-scale battery storage and interconnection investment to reduce dependence on historically vulnerable import routes.24

- Biomethane and green hydrogen. The role of green gases—biomethane in the near term and hydrogen in the medium and longer term—is being actively examined, particularly for hard-to-electrify sectors in industry and heating. Progress remains commercially uneven, and the business case for hydrogen at scale is still being assessed and established in most markets.25

- District heating and community grids. Heat networks remain significantly underdeveloped across much of Europe, given that they have the potential to play a large role in decarbonising residential and commercial heating.26 Scaling them up will require durable policy support and long-term investment signals, which a crisis environment makes harder to maintain.

- Carbon capture, utilisation and storage (CCUS). CCUS features in many national energy strategies, particularly as a bridging technology, but deployment remains below ambition and cost trajectories are uncertain.27

The most immediate reactions: affordability and competitiveness

In practice, the most visible near-term policy responses have focused not on accelerating decarbonisation but on cushioning the immediate economic impact of the shock—addressing affordability and competitiveness concerns for energy policymakers. Across Europe, planned, or potential, policy responses have included the following.

- Changes to the way wholesale electricity is priced (decoupling gas and electricity prices). The pricing of electricity may be driven by the price of gas, also with a high proportion of renewables-based generation in a country’s electricity mix. Under the current merit order model28, gas-fired generation sets the clearing price for electricity. This means that even in power systems with high shares of zero-marginal-cost renewables, the commodity price shock is nevertheless transferred in full to retail electricity bills (unless measures are adopted to prevent this). In April the UK published plans to reduce the impact of gas prices on electricity prices.29 In Italy, the DL Bollette (an energy Decree) has proposed a measure to reimburse Italian gas-fired plants for (part of) the costs that they incur in purchasing CO2 allowances under the EU ETS—its implementation will require prior approval from the European Commission under state aid rules.30

- Interventions at consumer level. Various countries have adopted consumer tax relief measures such as the reduction in fuel taxes in Germany31 or the temporary excise cut to road transport fuels in Italy.32 Retail price caps have recently been discussed and introduced, for example for heating oil in the UK.33 Measures have also been introduced to protect vulnerable consumers (e.g. to further subsidise electricity and gas for low-income households in Italy and to expand the scheme to district heating consumers).34

- Interventions to support industrial users. Specific measures have been introduced to target energy-intensive users (e.g. subsidies for industrial electricity use in Germany to prevent energy costs from driving deindustrialisation).35

- Policy reversal on major infrastructure decisions. One example is the coal exit in Italy, which has been delayed from 2026 to 2038.36 In Germany, some politicians are calling for the revival of previously decommissioned nuclear plants.37

- Role of gas. In the UK, calls to expand North Sea drilling licences—already present before the crisis—have intensified, with the argument that domestic gas production would directly increase near-term security of supply.38

The design of affordability interventions involves difficult trade-offs that policymakers must weigh up, including:

- the speed and administrative feasibility of delivery, which has often favoured broader measures compared to more targeted ones;

- the extent to which price signals that incentivise decarbonisation are preserved or suppressed;

- the case for targeting support towards those most in need, including vulnerable consumers;

- the case for targeting support towards strategically important industries where sustained cost pressures risk undermining investment and long-term competitiveness.

How these considerations are balanced ultimately requires judgement. The appropriate response will vary by country, by cost category, and by the nature of the shock being addressed.

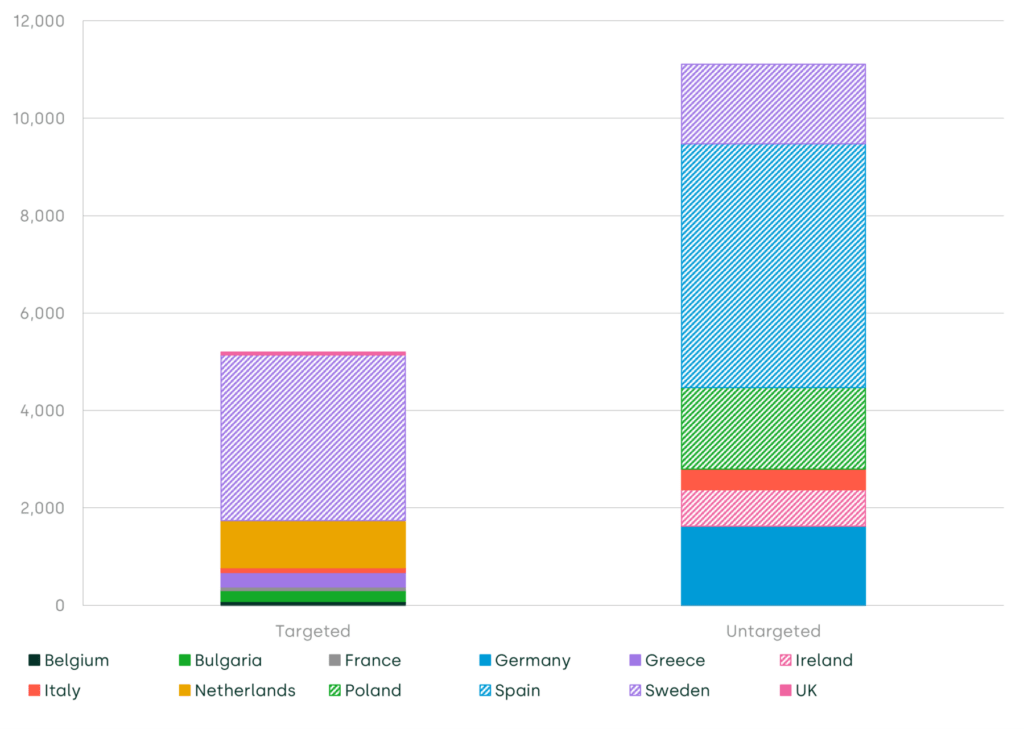

Targeting measures towards consumers or businesses with a greater need for support would reduce the concern about political interventions tending to reduce the incentive to decarbonise.39 However, a large share of financial support from measures introduced in Europe following the closure of the Strait of Hormuz seems to have been spent on untargeted measures, such as cuts to general energy excise duty or value added tax (VAT), which lack a clear target group. Figure 5 illustrates this based on a dataset of 30 fiscal measures across 12 countries.40 Around 70% of the spend on measures included in the dataset is on untargeted measures.

Figure 5 Fiscal measures by European country (€m)

Considering further trade-offs: the role of competitiveness in energy policy

At the EU level, the policy response has increasingly incorporated an industrial competitiveness dimension. Although this predates the current crisis, it has certainly been reinforced by it.

It is important to be clear about what ‘competitiveness’ means in this context, because it operates on two distinct levels. The first is the competitiveness of the EU’s energy supply chains—the extent to which the EU manufactures the clean technologies that it needs for the transition at home rather than depending on non-EU suppliers. The second is the competitiveness of those industries in the EU that use energy—in terms of the prices and reliability of energy as an input to manufacturing, chemicals, steel and other industries that compete on global markets or where the investment constraint effect of high energy costs is material, even if they mainly operate domestically. These two dimensions are related but distinct, and are addressed by different policies.

As discussed above, the second—protecting industrial users from high energy input costs—has been a focus of the most immediate crisis responses, such as Germany’s electricity subsidy for industrial users. But there is also an emerging European-level policy agenda aimed at building competitive domestic supply chains based on clean technology.

In particular, the Net Zero Industry Act (NZIA) and the subsequent NZIA Regulation41 are designed to ensure that a meaningful proportion of the clean technology needed for the transition is manufactured within the EU—reducing strategic dependence on non-EU suppliers and supporting the competitiveness of domestic industry. The framework also imposes mandatory non-price criteria in procurement procedures for clean technologies and renewable energy auctions, which have historically been focused on price. Key criteria are sustainability and resilience, the latter of which requires diversification of supply sources in case of high dependence. In the case of renewable energy auctions, non-price criteria must apply to at least 30% of the volume auctioned annually in each EU country (or at least 6GW per year per country).42

This agenda, however, is not just about supply-chain sovereignty. Investing in domestic renewable energy supply chains is also linked to industrial policy: it creates economic activity, supports high-value employment, and builds long-run capabilities in sectors that are likely to be central to global competition over the coming decades. Where localisation of clean-technology manufacturing also reduces the cost and increases the reliability of the energy input that broader industry depends on, this further increases the benefits. Oxera analysed these effects through different growth levers as drivers of decarbonisation, as well as economic growth, in our ‘Growth Zero’ report.43

This dual aim—treating energy transition as a strategy for both supply chains and long-run input costs—is also increasingly reflected in the duties of policymakers and regulators. In 2024, the UK government gave the energy regulator Ofgem an explicit mandate for economic growth.44 The Ofgem Review published in April 2026 proposes that this duty will be the first of three equal principal objectives: focusing on the interests of existing and future customers, net zero and economic growth.45 This is a significant move: it recognises that the energy regulator’s role is no longer ‘simply’ to protect consumers from excessive prices, but to actively support the conditions under which a competitive, low-carbon industrial economy can be built.

The Hormuz crisis has sharpened the political case for this localisation and industrial competitiveness agenda. The supply shock has hit energy costs and global trade flows at the same time, which has increased the policy and industry focus on the supply chain for clean technology.

A way forward? Maintaining focus under pressure

The energy trilemma has rarely been harder to navigate. The 2026 geopolitical tensions in the Middle East and the closure of the Strait of Hormuz have affected all dimensions of the trade-off simultaneously: security of supply is under threat, and affordability has deteriorated sharply for households and industry across Europe. At the same time, the window in which to make the investments necessary to meet climate commitments continues to narrow, while the political bandwidth to manage those investments is consumed by the immediate crisis.

The risk of reactive policymaking—a succession of individually motivated decisions that, in aggregate, undermine the coherence of national energy strategies—is real and present. Geopolitical instability increases policy uncertainty and tends to cause investors to delay long term investments. Policymakers need to carefully balance the different corners of the trilemma, and practical considerations. At the same time, competitiveness has emerged as an extension to the affordability objective of the trilemma. This includes the competitiveness of the EU’s own supply chain, and the competitiveness of energy-intensive sectors competing internationally and/or facing constraints in affording other costs (such as capital investments) due to high energy costs. The debate between ‘double down’ and ‘slow down’ will play out differently in each national context, depending on the country’s industrial structure and political economy, and how it is exposed to the shock. What is clear is that the decisions being made today—on coal phase-outs, renewable auction design, domestic fossil-fuel licensing, network investment and low-carbon technology subsidies—will define the shape of European energy systems for decades to come.

Footnotes

1 Global Counsel (2025), ‘A global view on the energy trilemma’, July, accessed 1 June 2026.

2 Clingendael International Energy Programme (CIEP) for DGTREN (2004), ‘Study on Energy Supply Security and Geopolitics’, Final Report, January, p. 37, accessed 1 June 2026.

3 Flues, F. and van Dender, K. (2017), ‘The impact of energy taxes on the affordability of domestic energy’, OECD Taxation Working Papers, 30, p. 10, accessed 1 June 2026.

4 Rosen, M.A. (2021), ‘Energy Sustainability with a Focus on Environmental Perspectives’, Earth Systems and Environment, 5, pp. 217–230, accessed 1 June 2026.

5 Butler, G., Mann, T., Jackson, P. and BBC Persian (2026), ‘Why the Strait of Hormuz matters so much in the Iran war’, BBC News, 8 April, accessed 29 May 2026.

6 Lipsky, J., Piasecki, B. and Yin, J. (2026), ‘The Iran oil shock may be different from other price spikes’, Atlantic Council, 18 March, accessed 22 May 2026.

7 Petroni, G. (2026), ‘European Gas Prices Soar After Qatar LNG Halt Jolts Market‘, The Wall Street Journal, accessed 22 May 2026; European Commission Joint Research Centre (2026), ‘How a prolonged Middle East crisis would impact energy prices and the EU economy. Macroeconomic modelling shows that EU inflation could rise to 3.5% in 2027’, News announcement, 27 May, accessed 1 June 2026; European Union Agency for the Cooperation of Energy Regulators (2026), ‘Key developments in European gas wholesale markets. Gas winter season 2025-2026’, 23 April, pp. 2–11, accessed 1 June 2026.

8 See, for instance, BBC (2026), ‘Why fuel and food prices could still be affected for months’, 8 April, accessed 12 June 2026.

9 Butler, G., Mann, T., Jackson, P. and BBC Persian (2026), ‘Why the Strait of Hormuz matters so much in the Iran war’, BBC News, 8 April, accessed 29 May 2026.

10 Carbon leakage refers to the potential that firms will transfer their production facilities (and thus the related emissions) to other countries with lower carbon taxes or emission standards.

11 Martini, L., Görlach, B., Kittel, L., Sultani, D. and Kögel, N. (2024), ‘Between climate action and competitiveness: towards a coherent industrial policy in the EU’, Ecologic Institute, December, p. iii, accessed 1 June 2026; Parry, I., Black, S., Minnett, D. and Zhunussova, K. (2025), ‘Policies to Decarbonize Industry While Addressing Competitiveness and Carbon Leakage’, CESifo Working Papers, 12272, accessed 1 June 2026.

12 World Economic Forum (2026), ‘The Strait of Hormuz crisis affects more than just oil. Here are 9 other commodities’, 1 April, accessed 22 May 2026.

13 Jao, N. (2026), ‘Oil and gas prices surge as Iran war disrupts Middle Eastern output’, Reuters, 2 March, accessed 26 May 2026; U.S. Energy Information Administration (2026), ‘International LNG prices rice amid Strait of Hormuz closure’, 28 April, accessed 26 May 2026; European Union Agency for the Cooperation of Energy Regulators (2026), ‘Key developments in European gas wholesale markets. Gas winter season 2025-2026’, 23 April, pp. 2–3, accessed 1 June 2026.

14 European Commission (2026), ‘Statement by President von der Leyen on the impact of the situation in the Middle East on the European Union’, 13 April, accessed 1 June 2026.

15 European Commission (2026), ‘Communication from the Commission to the European parliament, the Council, the European economic and social committee and the Committee of the regions. AccelerateEU – Energy Union. Affordable and Secure Energy through Accelerated Action’, COM(2026) 370 final, 22 April, accessed 1 June 2026.

16 Weise, Z. (2026), ‘EU countries to call for faster green transition over Iran fuel crisis’, Politico, 15 April, accessed 22 May 2026.

17 Moscovici, A. and Nguyen, P.-V. (2026), ‘War in Iran: the long-awaited electroshock for the European energy transition?’, Institut Jacques Delors, 9 April, accessed 22 May 2026.

18 European Commission (n.d.), ‘National long-term strategies’, accessed 22 May 2026; European Council and Council of the European Union (n.d.), ‘European Green Deal’, accessed 22 May 2026.

19 European Commission (n.d.), ‘National long-term strategies’, accessed 22 May 2026.

20 Elliott, C., Schumer, C., Gasper, R., Ross, K. and Singh, N. (2024), ‘A Sustained Portfolio of Policies Have Transformed Denmark’s Power Sector’, World Resources Institute, 6 March, accessed 22 May 2026.

21 World Economic Forum (2015), ‘How Denmark is driving the transition to clean energy’, 19 March, accessed 22 May 2026; Agora Energiewende (2023), ‘Variable Renewable Energy Grid Integration’, accessed 1 June 2026.

22 Ptak, A. and Strzałkowski, P. (2026), ‘CLEW Guide – Poland stumbles through energy transition with uneven progress and political headwind’, Clean Energy Wire, 24 April, accessed 22 May 2026; Czyzak, P. (2024), ‘Changing course: Poland’s energy in 2023’, Ember, 7 March, accessed 1 June 2026.

23 World Nuclear Association (2026), ‘Economics of Nuclear Power’, 24 March, accessed 22 May 2026.

24 European Commission (n.d.), ‘Electricity interconnection targets’, accessed 22 May 2026; Yanatma, S. (2026), ‘Europe’s electricity storage race: Which countries lead in battery capacity?’, Euronews, 8 May, accessed 22 May 2026; European Commission (n.d.), ‘REPowerEU – 4 years on’, accessed 22 May 2026.

25 European Commission (n.d.), ‘Hydrogen’, accessed 22 May 2026; H2Inframap (2026), ’Hydrogen Infrastructure Map’, accessed 22 May 2026; European Commission (n.d.), ‘Hydrogen and decarbonised gas market’, accessed 22 May 2026; European Court of Auditors (2024), ‘The EU’s industrial policy on renewable hydrogen – Legal framework has been mostly adopted – time for a reality check’, Special Report 11/2024, 16 July.

26 Sneum, D.M., Billerbeck, A., Kachirayil, F. and McKenna, R. (2025), ‘Barriers to district heating deployment: insights from literature and experts’, Energy Policy, 206, pp. 1–26.

27 Fajardy, M., Greenfield, C. and Rosales, P. (2026), ‘Policy and financing momentum sustain CCUS progress despite setbacks’, International Energy Agency, 27 March, accessed 22 May 2026; International Energy Agency (2026), ‘Energy Technology Perspectives 2026’, April.

28 In this system, demand is met by ranking the electricity generator supply bids in ascending order based on their marginal production cost required to produce an additional unit of electricity. See, for instance, European Commission (2023), ‘The Merit Order and Price-Setting Dynamics in European Electricity Markets’, accessed 2 June 2026.

29 UK Government (2026), ‘Decisive action to break influence of gas on electricity prices’, News story, 21 April, accessed 22 May 2026.

30 Normattiva, ‘Decreto-Legge 20 febbraio 2026, n. 21, convertito con modificazioni dalla L. 10 aprile 2026, n. 49 (in G.U. 18/4/2026, n. 90)’, article 6, accessed 22 May 2026. For a broader discussion on the measure see Macchiati, A., Belforti., C. and Vitelli, R. (2026), ‘Il rimborso della CO2 previsto dal “DL Bollette”: quale impatto?’, 18 March, Staffetta Quotidiana.

31 Bundesregierung (2026), ‘Governing coalition agrees on rapid aid for consumers and the economy’, 13 April, accessed 22 May 2026.

32 Gazzetta Ufficiale (2026), ‘DECRETO-LEGGE 18 marzo 2026, n. 33’, accessed 22 May 2026.

33 UK Government (2026), ‘Over £50 million to help families struggling with soaring heating oil costs’, News story, 16 March, accessed 22 May 2026.

34 Normattiva (2026), ‘Decreto-Legge 20 febbraio 2026, n. 21, convertito con modificazioni dalla L. 10 aprile 2026, n. 49 (in G.U. 18/4/2026, n. 90)’, article 1 and article 1-bis, accessed 22 May 2026.

35 European Commission (2026), ‘State Aid SA.120495 (2026/N) – Germany. CISAF – Temporary electricity relief for energy-intensive users. C(2026) 2584 final’, 16 April, accessed 1 June 2026; Wehrmann, B. (2026), ‘EU approves German industry electricity price, companies say more relief needed’, Clean Energy Wire, accessed 22 May 2026.

36 Ibid., article 5-bis; Reuters (2026), ‘Italy to postpone shutdown of coal-powered plants by 13 years’, 31 March, accessed 22 May 2026. The coal phase-out was previously expected by January 2026, except in Sardinia, where it was expected by 2028.

37 Tagesschau (2026), ‘Spahn will Debatte um AKW-Reaktivierung’, 16 April, accessed 22 May 2026.

38 OEUK (2026), ‘UK energy industry leaders respond to worsening energy crisis’, 20 May, accessed 22 May 2026.

39 OECD (2022), ‘Why governments should target support amidst high energy prices’, 30 June, p. 1, accessed 1 June 2026.

40 Based on Bruegel (2026), ‘2026 European energy crisis fiscal response tracker’, Excel download, accessed 20 May 2026. The dataset does not represent an exhaustive list—according to Bruegel’s description, measures without a clearly defined budget or that are budget-neutral are not captured. For instance, all measures of the Italian DL Bollette are missing. The European Commission has also published a list of measures, although without capturing the fiscal spend: European Commission (2026), ‘Overview table of national emergency measures adopted by EU Member States since 28 February 2026’, 19 May, accessed 1 June 2026.

41 European Commission (n.d.), ‘The Net-Zero Industry Act’, accessed 22 May 2026; European Parliament and European Council (2024), ‘REGULATION (EU) 2024/1735’, 17 August, accessed 1 June 2026.

42 European Commission (n.d.), ‘The Net-Zero Industry Act’, accessed 22 May 2026.

43 Oxera (2024), ‘Growth Zero’, accessed 9 June 2026.

44 GOV.UK (2024), ‘Growth duty’, 24 May, accessed 9 June 2026.

45 GOV.UK (2026), ‘Ofgem Review: final report’, 22 April, accessed 9 June 2026.

Contact

Carlotta von Bebenburg

Senior ConsultantContributors

Related

Related

No water, no growth: tackling inefficient business water demand

Water is not typically thought of as a constraint on economic growth in England. Yet that is precisely what it is becoming. Commercial growth and new developments are being turned away because there is insufficient water to serve them. Some water companies are already exercising their powers to refuse… Read More

Oxera responds to the European Commission’s consultation on its Draft Merger Guidelines

We welcome the Commission’s work to consolidate more than two decades of decisional practice, economic analysis and case law into a single framework. The draft is a strong foundation for future merger enforcement, particularly in its treatment of non-price competition, efficiencies and the broader assessment of competitive effects. Read More