Access to land for mobile telecoms networks: a framework for negotiation and regulation

Mobile towers serve as the backbone of mobile telecoms networks, hosting radio access network equipment that enables us to receive calls, texts and to access the internet on our mobile devices. In turn, the ability of the builders of mobile towers to access land—whether that is on the ground, a rooftop or street furniture—to build this infrastructure in strategic locations is critical to deploying a well-functioning mobile network that serves consumers wherever they want to use their device. In short, no access to land in a particular area means no mobile towers, which ultimately results in poorer mobile connectivity for consumers.

Historically, land access negotiations involved thousands of individual landowners, many of which controlled a single site. But the emergence of ‘land aggregators’—investment firms that acquire portfolios of site access rights—is reshaping these dynamics. This consolidation creates both opportunities and risks. Where the risks crystallise in adversarial negotiations between aggregators and access-seekers, as has recently occurred in France (see the box below), this can result in bad outcomes for industry and consumers. These outcomes include costly disputes, increases in fees to access land, power to sites being switched off, and even the eviction of mobile network operators (MNOs) and tower companies (TowerCos) from sites, with resulting losses in mobile services for customers.

Regulators are only just beginning to grapple with these issues in a meaningful way. At an EU level, the Gigabit Infrastructure Act (GIA) and draft Digital Networks Act (DNA) provide light-touch protections that do not constrain some of the more problematic practices. It remains to be seen whether the outcomes of the European Commission’s 2025 consultation on guidance on the application of the GIA will provide stronger protections for land access-seekers. Meanwhile, in the UK, the Electronic Communications Code (ECC) (2017) has proven successful in reducing access prices, but may affect the incentives of land owners to engage in negotiations.

In this article, we analyse the economics of land access and assess the potential for the emergence of land aggregators to create a new hold-up problem that warrants further regulatory intervention. In doing so, we propose a framework to assist both the industry players involved in these negotiations (MNOs, TowerCos, and land aggregators) and regulators in considering whether to intervene in the land access market or how to resolve disputes when called upon to do so.

The ultimate bottleneck?

Land access sits at the foundation of mobile network deployment. As Figure 1 below illustrates, without land or rooftop space to host infrastructure, the entire value chain, from passive towers to active equipment to the radio spectrum itself, cannot function. If the value chain does not function, the end-consumer will not receive a mobile service. As such, access to land represents an economic bottleneck.

Figure 1 Mobile network value chain

Not all sites are created equal, and there is no single ubiquitous land owner. While governments and local authorities may be key access providers to sites in some areas, in other cases each site might have a different owner. This could be a farmer (e.g. of a field), a commercial real estate owner (e.g. of an office or factory, or the freeholder of a block of flats), or a private real estate owner.

Overcoming this potential economic bottleneck therefore requires TowerCos and MNOs to navigate a fragmented landscape by entering into negotiations with many separate parties. This fragmentation creates inherent inefficiencies.

Land aggregators provide a possible solution to this inefficiency.

The emergence of land aggregators: a new power dynamic

Land aggregators are investment firms that purchase or lease the land (or rooftop space) on which a mobile tower is built (or will be built). Their typical financial model—as set out in Figure 2 below—is to purchase the rights to the land from the owner via a lump sum payment, taking control of the relationship with the owner of the mobile tower, from which they receive regular rental income (instead of the land owner, as in the traditional model set out in Figure 3 below).1 They can then aggregate and consolidate long-term land access rights into a larger portfolio of land.

Figure 2 Land access relationship with a land aggregator

Figure 3 Traditional land access relationship

Land brokers are another route through which a third party forms a relationship with the land/rights owner, and thus can influence the terms over which access-seekers (including TowerCos and MNOs) are able to gain access for deploying (or maintaining) telecoms infrastructure on the site. In the rest of this article, for ease of reference, we refer to parties that take over the relationship with the MNO or TowerCo as ‘land aggregators’, without distinguishing between those that take full ownership (land aggregators) and those that only take over the relationship (land brokers).

Land aggregators can, in principle, solve the fragmentation problem and bring significant benefits to the industry by providing long-term certainty to both sides: landowners receive upfront payments, eliminating renewal risk, while network operators gain simplified administration when dealing with a single counterparty across multiple sites rather than hundreds of individual landowners.

If this enables an increase in the supply of land for telecoms infrastructure (by ‘unlocking’ the value of the site by bringing forward future payments into an upfront lump sum and enabling it to be invested elsewhere), and improved efficiency by streamlining land access negotiations so that access-seekers have to negotiate with only one counterparty rather than multiple individual landowners (effectively reducing the transaction cost for the access-seeker), it could result in positive outcomes by accelerating roll-out and, ultimately, the network quality experienced by mobile consumers.

However, there has been some concern within the mobile industry that land aggregators are leveraging their position in the land access market in order to take advantage of this economic bottleneck either by increasing access prices or by pushing access-seekers off the land. The situation in France—which we discuss in the box below—is a good illustration of the negative outcomes that could result from aggressive land aggregator behaviour.

The degree to which land aggregator behaviour creates problems can be assessed through two economic frameworks:

- the bargaining power framework (examining how control of site portfolios shifts negotiating positions and can result in ‘hold-up’ problems);

- dynamic considerations (examining how sunk investments may affect investment incentives).

We address each of these in turn.

The economics of land access: a bargaining power framework

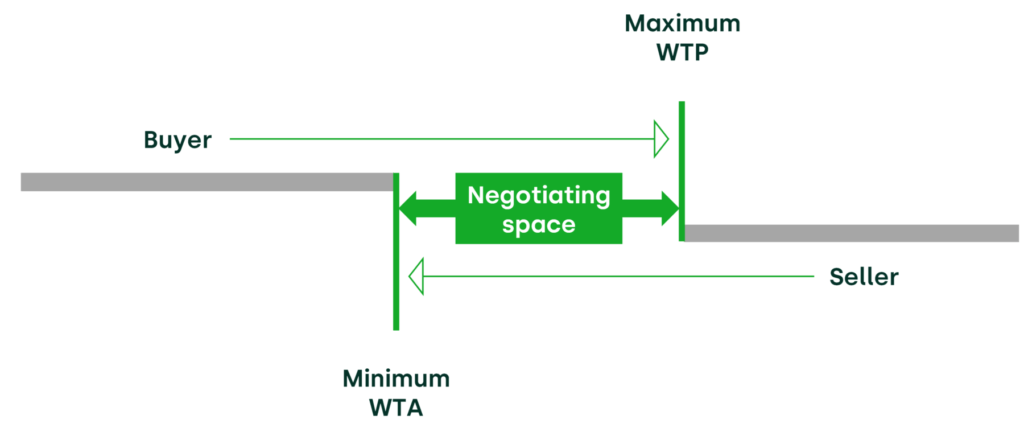

Consider a typical negotiating framework between a land owner seeking to sell access to its land, and an access-seeker (TowerCo) wishing to gain access to the land or retain access to it through a contract renewal negotiation.

Under the bargaining power framework, the negotiating space between the land provider and access-seeker is determined by the parties’ respective willingness to accept (WTA) and willingness to pay (WTP). These represent the minimum amount of money that the land provider is willing to accept to give access to its land, and the maximum amount that the access-seeker is willing to pay to gain (or retain) access to the land.

- A land provider’s WTA is determined by factors such as whether the land provider has alternative uses for the land (for example, for agricultural land, their WTA might be only marginally above expected farming income, whereas for commercial rooftop space, their WTA would reflect the opportunity cost of alternative uses), and their experience of land access price negotiations.

- An access-seeker’s WTP is likely to be determined by factors such as whether the land accommodates an existing site or is required for a new build, the characteristics of the site location (for example, whether there is a heavy footfall of mobile users nearby, or whether it is critical to supporting network coverage) and the extent to which there are alternative locations on which to build the site. For a new build with multiple feasible locations, their WTP will be much lower than for an existing site with a large sunk investment, or a location that is essential for meeting coverage targets.

The negotiating space between WTA and WTP within this framework is depicted in the figure below.

Figure 4 Negotiating framework

Economic theory suggests that, with balanced bargaining power, the agreed price could fall anywhere within this range, with the specific outcome being determined by relative negotiating skill.

The bargaining position of the landowner strengthens significantly when:

- the site is necessary for the MNO to gain/retain a certain level of mobile coverage, either for commercial reasons or to comply with coverage obligations imposed by the regulator;

- the site is necessary to provide network capacity, such that moving the site to an alternative location would leave an area where high customer demand is unserved or under-served;

- there are no viable alternative locations within the area for the site to be relocated to—for example, due to planning restrictions.

A key consideration for both parties is that mobile sites require substantial one-off investments (planning permission, backhaul infrastructure, network integration) that have little value if the site must be relocated. Once these investments are sunk, the TowerCo/MNO’s WTP for land access will increase dramatically. The switching cost of relocating an established site is likely to far exceed the alternative use value of the land. This creates a hold-up problem whereby the land provider knows that the access-seeker has a sunk investment that it will be reticent to walk away from, thereby increasing the land provider’s bargaining position, for example upon contract renewal. This hold-up problem is likely to be more pervasive when land aggregators control multiple sites and are negotiating access for them with the same counterparty, since a TowerCo or MNO might relocate one or two sites under duress, but cannot simultaneously relocate dozens without a significant impact on network quality.

More generally, land aggregators are likely to have more dominant negotiating positions vis-à-vis access-seekers than other land providers. This is because, by owning a multi-site portfolio, they reduce the outside options (the alternative site locations) that the access-seeker has available to it when negotiating access to a specific site. The access-seeker also knows that it is likely to have to negotiate with the same land aggregator for access to sites in other locations, meaning that, if it does not meet the WTA of the land aggregator on one site, this may affect the success of negotiations elsewhere. Moreover, land aggregators are likely to be more sophisticated negotiators than other land providers with a better idea of the value of the land—due to the fact that this is precisely their business—further improving their negotiating position.

Alternatively, the access-seeker could hold a dominant bargaining position if (i) the land provider is uninformed about the value of its land; (ii) there are realistic alternative locations to host a site; and/or (iii) the site had relatively low sunk investment costs.

Under these circumstances, there may be scope for one of the parties to exploit its bargaining position, resulting in sub-optimal societal outcomes. For example, if a land aggregator holds a large enough bargaining position, it could require an ‘excessive’ rent for access to the land. This could subsequently lead to poor outcomes in the mobile ecosystem, for example if the increased cost is passed on via higher mobile prices or reduces a MNO’s investment in its network, to the detriment of quality of service.

Introducing dynamics: why site-specific investment changes everything

The static bargaining framework set out above is missing a critical dynamic dimension—the impact on the incentives to invest in mobile sites.

As we discuss above, TowerCos and MNOs incur large investment costs when deploying their mobile sites. Importantly, these are costs that cannot easily be recovered if the site is subsequently moved to another location. This creates a hold-up problem whereby land owners can leverage this bargaining position to demand large rents for access to land when land access contracts are renegotiated.

Importantly, the hold-up problem can create inefficiency even outside of contract renegotiations.

This is because sophisticated TowerCos and MNOs may anticipate that land owners could engage in aggressive lease renegotiation in the future, risking a situation where they need to move to another site and duplicate their large sunk investment should renegotiations fail. This may result in them under-investing in site-specific infrastructure, deploying lower-quality equipment, or avoiding deploying sites altogether in areas where they consider there to be the highest risk—for example, where they consider that land aggregators are likely to be present in the future.

This dynamic inefficiency could have serious implications for mobile networks and, ultimately, consumers. For example, the cost to consumers may be that investment in 5G non-stand-alone (NSA), 5G stand-alone (SA) or 6G upgrades does not happen as extensively, coverage improvements are delayed, and/or network densification is scaled back—all because operators rationally anticipate aggressive lease renegotiation from certain counterparties.

The risk from land aggregators in practice

As we discuss above, the potential downsides associated with land aggregators are typically driven by the additional bargaining power that land aggregators can obtain from combining the access rights to multiple sites. In some circumstances, this additional bargaining power is alleged to have allowed land aggregators to increase land access rental prices. In other places, it may disincentivise network roll-out as TowerCos and MNOs anticipate future issues.

When things go wrong: Valocîme, France

A notable example of the possible frictions between land aggregators and MNOs/TowerCos has recently been playing out in France. The land aggregator and aspiring TowerCo Valocîme entered the French market in 2017 and began acquiring the rights to land on which mobile towers were located. It has since also sought to acquire the existing tower infrastructure on the land at ‘construction price’, including by applying for eviction notices—with some success—and ultimately cutting power to sites where TowerCos do not comply with its demands.1 Valocîme’s ultimate objective appears to be to increase the rents paid by mobile operators to access the infrastructure on the land.2 However, to date, MNOs have resisted contracting with Valocîme. This has resulted in a dispute before the French telecoms regulator, ARCEP, where Valocîme sought for the MNOs to be required to enter into negotiations to access the land to which it owns the rights.3 ARCEP ultimately dismissed Valocîme’s requests. The result of this has been a number of legal battles involving ARCEP, the French government and the Court of Appeal. Industry commentators consider that this ‘telecoms war’ has had negative consumer outcomes—for example, through network outages following Valocîme’s decision to switch off power to mobile sites—and threatens to slow infrastructure upgrades.4

Note: 1 Capacity (2025), ‘News: France’s tower lease war’, 21 February. 2 Euractiv (2025), ‘French court throws shade at government’s proposed telecoms land-restriction rule’, 18 February. 3 Arcep (2025), ‘Dispute Settlement: Arcep denies Valocîme requests, settling its disputes with mobile telephony operators Bouygues Telecom, Orange and SFR, respectively’, press release, 1 January. 4 Capacity (2025), ‘News: France’s tower lease war’, 21 February.Source: Oxera.

The possibility of such situations arising is not just theoretical. In fact, this is precisely what appears to have occurred in France, where land aggregator Valocîme implemented aggressive lease renegotiation tactics, including switching off power to sites, demonstrating the credibility of its hold-up threat (see the box below).

The regulatory dilemma

The extent to which the potential issues identified above exist is critical to understanding how the increased presence of land aggregators may affect industry outcomes. In some circumstances they may affect the scope, scale and timing of network upgrades (e.g. upgrades to 5G NSA, 5G SA or 6G), densification (e.g. building more sites within an area to improve speeds received by customers) and even MNOs’ ability to meet their own coverage or quality targets or regulatory obligations (e.g. coverage obligations).

Given the incentive and ability of some land aggregators to take advantage of instances where they hold dominant bargaining positions, it is important to assess what protections are available to land access-seekers today.

Today’s regulatory framework: varying protections for access-seekers

We are unaware of any abuse of dominance cases brought against land aggregators from a competition law perspective. This may be because there have not yet been any clear-cut cases (even if the potential for abuse is there). However, one can also imagine the complexities associated with bringing a successful case, given that a focus on specific site locations may reflect difficulties in defining local markets or ascribing market power in those markets. In any case, in the presence of hold-up concerns, ex post intervention through the courts may be too slow and poorly suited to preventing sunk cost exploitation—as, by the time the hold-up occurs, the harm is already done.

We therefore expect regulators and/or parties affected by land aggregators’ practices to turn to ex ante regulation if they consider there to be a problem.

Today’s ex ante regulation varies somewhat across jurisdictions. In the EU, the ex ante protections currently afforded to access-seekers are fairly light. The GIA seeks to promote joint use of existing infrastructure to facilitate the provision of very high-capacity networks by requiring ‘good faith’ negotiations between land owners (or parties operating on their behalf) and operators, including in relation to price.2 However, ‘good faith’ is inherently difficult to define and enforce.3 For example, what constitutes unreasonable pricing when switching costs are high? In its recently published draft DNA, the Commission proposes to require that fees for access to land be ‘objectively justified, transparent, non-discriminatory and proportionate in relation to their intended purpose […].’4

The UK, however, is an example of a country that has taken a more interventionist approach to regulating access to land, in this case via the requirements in the UK’s ECC (and the subsequent Product Security and Telecommunications Infrastructure, PSTI, Act 2022, which extends rights of telecoms operators under the ECC).5 However, as the box below details, while this intervention has achieved its primary objective—dramatically reducing land access costs—it could create some unintended consequences that offer lessons for other regulators.

The UK Electronic Communications Code

In 2017, the UK updated its land access rules with reform of the ECC. Two key impacts of the updated ECC were as follows.

1.By moving away from market-based land valuations to a valuation approach based on the assumption that the ‘transaction does not relate to the provision or use of an electronic communications network’1—effectively basing the access fee on the next highest valuation of the land, which is typically significantly lower than its value to telecoms operators—the ECC reduced the rental costs paid by telecoms operators to land access providers.

2.It introduced ‘Code rights’ that gave telecoms operators improved rights to access land to upgrade and share their equipment without incurring additional costs.

The impact of the ECC on land access prices appears to have been significant. Some reports suggest that access prices have fallen considerably—to 15–20% of pre-2017 levels2—following the update to the ECC.

While operators welcomed lower costs from this price reduction, the lower rents plus some strengthening of code rights in favour of telecoms operators, under the PSTI Act, can alter landowners’ incentives to provide access. For example, as noted by the Department for Culture, Media and Sport:3

Although the introduction of the statutory valuation framework in the 2017 Code reforms has reduced deployment costs for operators, we recognise that this has had an impact on the willingness of occupiers and site providers to agree, or renew, Code rights.

While it was reported that there could also be a resulting increase in litigation between land access-seekers and providers4 (which would have a potential knock-on impact on the speed at which access terms are agreed, potentially undermining some of the intended benefits of the ECC), this appears to have been limited in practice. We understand that there is a high rate of consensual agreements between infrastructure providers and site providers, without litigation. For example, since the PSTI Act was implemented in 2022, only 39 renewals have required court hearings, with over 60% of those cases being raised by a single land aggregator.5 However, landowners may still feel disgruntled about the erosion of the value of telecoms leases.

Note: 1 Communications Act 2003, Schedule 3A, Part 4, para. 24(3)(a). 2 See Farmers Weekly, ‘How legislation affects rural telecoms mast landlords’, 13 January. 3 Department for Culture, Media and Sport (2021), ‘Access to land: consultation on changes to the Electronic Communications Code-government response’, 24 November, para. 3.7. 4 See APWireless (2022), ‘APWireless – submission to the Commons Bill Committee of the Product Security and Telecommunications Infrastructure Bill’.5 Mobile Infrastructure Forum (2025), ‘Press release: 5G rollout at risk – MIF welcomes Government Consultation while highlighting urgent need to fully deal with 6,200 sites stuck in legislative limbo’, 20 May. Source: Oxera.

The UK experience demonstrates that price interventions, even when reducing costs, have the potential to distort incentives and increase transaction costs through other channels. This highlights the need to ensure that regulatory interventions are tightly focused on the harms that they are aiming to remedy.

A framework for regulatory assessment

The land aggregator model, and its impact on land access negotiations, presents regulators with a genuine dilemma. Although there is evidence of some land aggregator behaviour resulting in sub-optimal market outcomes (for example, in France), there is currently limited evidence that this is a systemic issue that requires widespread regulation—indeed, we see evidence of continued network roll-outs across jurisdictions, which may be indicative of a well-functioning market. Meanwhile, interventions that can be successful in reducing access prices should be carefully considered alongside any unintended consequences.

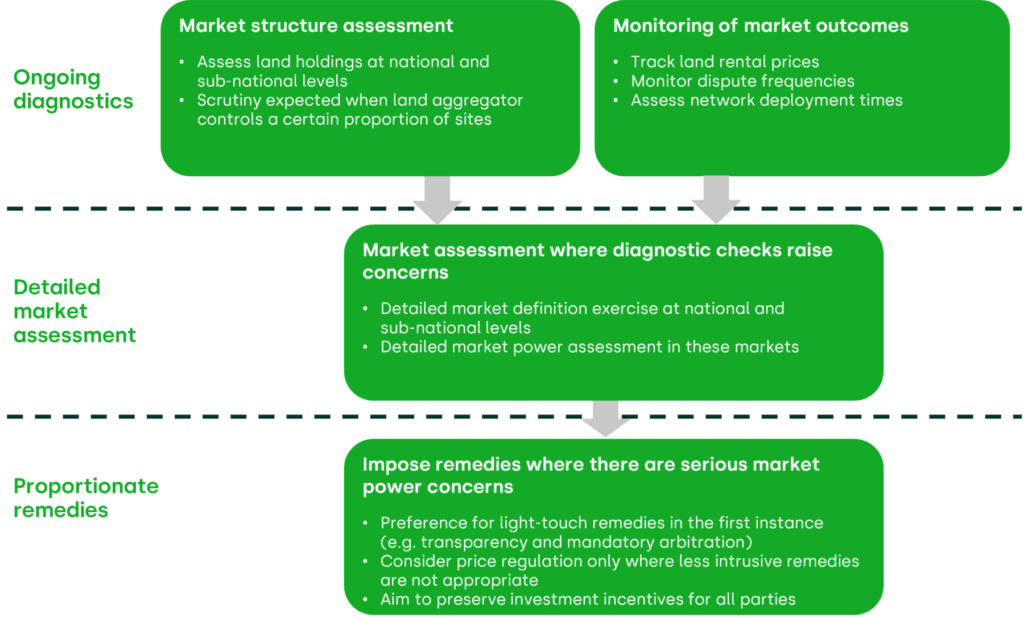

We propose a three-stage framework for regulatory assessment (as illustrated in Figure 5 below).

- Stage 1: ongoing diagnostics: monitor market indicators to identify whether problems are emerging

- Stage 2: detailed market assessment: if diagnostics raise concerns, conduct rigorous analysis to understand the scope and scale

- Stage 3: proportionate remedies: select interventions that address identified problems while preserving investment incentives

This sequential approach avoids both premature intervention (regulating before problems materialise) and delayed response (waiting until there is substantial harm).

Figure 5 Proposed land aggregation assessment framework

This framework recognises that there may not be a systematic issue with land aggregators—in fact, as we discuss above, they can bring benefits to mobile telecoms markets. Therefore, as a first step, we recommend that the regulator undertakes ongoing diagnostic checks of the market to assess whether there appear to be any issues and, if so, how and where they present themselves.

If the initial diagnostic approach uncovers possible issues, the regulator’s role would then be to undertake a detailed market definition and market power assessment to understand the scope and extent of any issues. Once this task is complete, it should select the appropriate remedies that proportionately solve the market failure identified, while seeking to retain land provider and access-seeker investment incentives.

Any regulatory intervention must balance competing objectives: preventing exploitation of MNO/TowerCo sunk investment, yet maintaining landowner incentives to provide access and preserving aggregator business models where they add value. It is also essential to avoid deterring network investment through regulatory uncertainty. Over-regulation risks discouraging land aggregators from entering markets where they could provide genuine efficiency benefits, while under-regulation risks hold-up problems that could slow or even preclude network deployment.

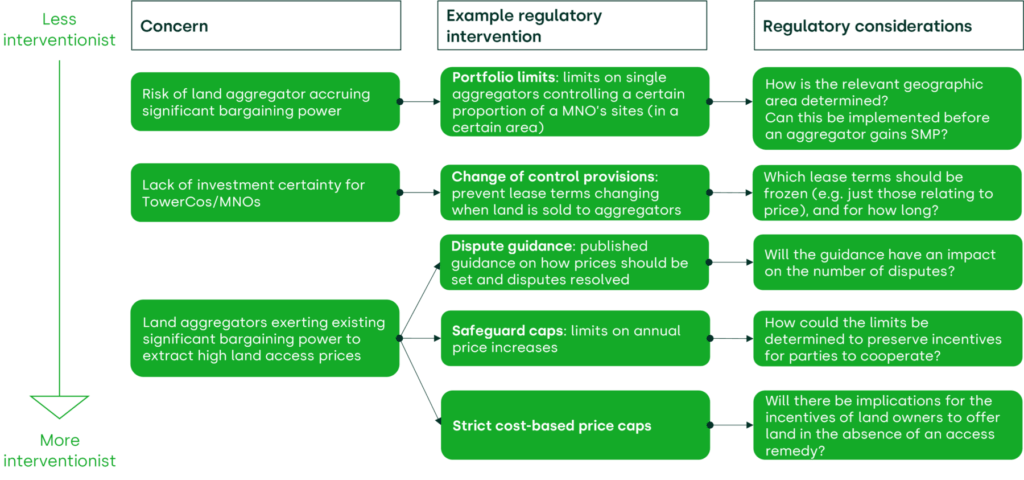

In this context, a range of interventions are available in a regulator’s toolkit, with different levels of intrusiveness should they uncover pervasive issues. The appropriate intervention will be informed by the specific situation. In Figure 6 below we present a range of example interventions that vary by their level of intrusiveness and the situation to which they are most applicable. Different regulatory interventions and considerations are required depending on whether the concern is the risk of land aggregators accruing significant bargaining power due to land accumulation; lack of investment certainty for TowerCos and MNOs due to potential changes in lease terms after change of land ownership; or the risk of excessively high land access prices.

Figure 6 Example regulatory interventions

As a light-touch intervention, the role of clearer dispute resolution guidelines or the establishment of specialist dispute resolution bodies should not be dismissed. If dispute resolution is left to the civil courts or general arbitration courts, this can add significant delays, and even inconsistent outcomes that lead to uncertainties in how disputes will be handled. Rules that provide a clear framework and timelines and are assessed by a specialist body (or the telecoms regulator, as in the Netherlands with the ACM6) can provide greater clarity and certainty for both sides, which can itself facilitate and accelerate consensual agreements between parties.

Conclusions, and implications for industry

Access to land is critical to the mobile industry. In particular, it is necessary in order to (i) upgrade mobile networks to be compatible with new technologies; (ii) densify networks to meet increasing consumer demand for data (for example, as mmWave spectrum is deployed); and (iii) improve mobile coverage to meet consumer expectations that they can access mobile data wherever they choose. The land access question will only grow more critical as these trends continue in the future.

Land aggregators are not inherently problematic. They can provide valuable services: long-term certainty for landowners, simplified negotiations for operators, and efficient capital allocation. But portfolio consolidation, combined with site-specific sunk investment, creates genuine hold-up opportunities—as France’s Valocîme case vividly demonstrates. The question is whether such cases represent isolated incidents or systemic problems. Current evidence is mixed. While dramatic disputes attract attention, network deployment is continuing across markets. Furthermore, the UK’s experience shows that some interventions can create new problems while solving old ones.

The strategic imperatives that emerge from the current situation appear to be as follows.

- MNOs and TowerCos need to think strategically about how they plan their networks and negotiate access to land in a world where their bargaining power relative to some land providers may be diminishing and where the threat of hold-up is increasing. If they have significant concerns, and where sites are critical (e.g. to deliver coverage obligations), purchasing land outright themselves may be justified despite the costs associated with doing so.

- Land aggregators must be conscious that business models based on portfolio leverage, hold-up exploitation and/or aggressive pricing will attract regulatory attention. Sustainable approaches that genuinely provide long-term certainty to both landowners and network operators can add value and will be well received in the industry.

- Regulators must assess whether the shift towards aggregated control of land access creates systemic problems requiring new regulatory intervention, or whether existing frameworks (contract law, competition law, sector-specific ‘good faith’ obligations) are sufficient. The answer is likely to vary by market and at the sub-national geography level. We therefore propose that systematic monitoring now, using the diagnostic framework outlined above, would be advisable. If intervention proves necessary, lighter-touch remedies (transparency, arbitration, contractual protections) should be exhausted before price regulation is considered.

Footnotes

1 APWireless, ‘Benefits Of A Lease Premium’, accessed 2 February 2026.

2 European Commission (2024), ‘Regulation (EU) 2024/1309 of the European Parliament and of the Council of 29 April 2024 on measures to reduce the cost of deploying gigabit electronic communications networks, amending Regulation (EU) 2015/2120 and repealing Directive 2014/61/EU (Gigabit Infrastructure Act)’, 29 April, Recital 15, Article 3.

3 This phrasing is also less precise than what was originally proposed for Article 3 of the GIA, which stated: ‘Where necessary to ensure the continuity of the electronic communication service, owners of land on which associated facilities have been installed with a view to deploying elements of very high capacity networks, shall negotiate with undertakings that provide or are authorised to provide those associated facilities under fair and reasonable terms and conditions, and in accordance with national contract law, on the access to such land, including the price for such access.’See European Parliament (2003), Report A9-0275/2023.

4 European Commission (2026), ‘Proposal for a regulation of the European Parliament and Council on digital networks, amending Regulation (EU) 2015/2120, Directive 2002/58/EC and Decision No 676/2002/EC and repealing Regulation (EU) 2018/1971, Directive (EU) 2018/1972 and Decision No 243/2012/EU (Digital Networks Act)’, 21 January, Articles 62–64.

5 Including code rights in relation to landowner control, rights to access specific infrastructure, and rules for resolving disputes.

6 The ACM has the power to settle disputes under the Dutch Telecommunications Act (Tw). See, for example, Authority for Consumers and Markets (2024), ‘ACM mandates Aegon to accept joint use of antenna site on its building in Alphen aan den Rijn’, 3 October.

Download

Contact

Harvey Nash

Managing ConsultantContributors

Related

Download

Related

What is venture capital, how does it work, and what are the risks?

In the third and final episode demystifying private equity, we explore the world of venture capital. While venture capital has delivered exceptional returns for some investors and founders, it’s also very high risk. So, is vibrant venture capital essential for economies seeking to boost innovation and drive productive growth? In… Read More

Measuring and inferring anticompetitive effects from an exchange of information

In four rulings1 dated 3 November 2025, the Spanish National Court overturned the Decision of the Comisión Nacional de los Mercados y la Competencia (CNMC) in case S/DC/67/17 Tabacos2 (‘the Decision’). These four rulings are significant because they close one of the first cases that the… Read More