Boosting growth, competitiveness and productivity in the EU and UK

Low economic growth is a current challenge for most major European economies, especially given the new fiscal burden of increased defence spending. Funding social challenges—such as climate change, the digital transition and European security—requires either some parts of society to be worse off, or that economies generate new sources of economic growth. But where is the necessary future growth to come from? There is a need to improve competitiveness, and while removing regulatory frictions or infrastructure investment may assist, the major contribution will be from the growth of new industries to boost productivity. This article considers how that growth will be financed, and where it will likely occur.

Introduction

’Europe has been worrying about slowing growth since the start of this century. Various strategies to raise growth rates have come and gone, but the trend has remained unchanged.’ This is the opening sentence of the foreword to the Draghi report on European competitiveness.1 This article continues from a previous Agenda article2 that used the UK as a case study to analyse underlying causes and official responses. In this article, we consider the possible European institutional responses directly, followed by any implications for the UK. These two markets, the UK and the EU, are interconnected, and indeed the UK is a source of venture capital for the EU, and the EU is a major potential market for the UK for growing industries and defence products. Both face similar challenges and are developing responses in similar directions.

Draghi’s vision: the EU’s new approach

The Draghi report explains that the EU did not benefit from the digital revolution to the extent of the US. It also states that the EU is weak in related emerging technologies, highlighting that only four of the top 50 technology companies3 are based in the EU. For the past 20 years, the top three investors in research and development (R&D) in Europe were automotive-focused (in the US, it was automotive and pharmaceutical), but now the top three R&D investors, globally, are all tech companies. It is necessary to trace this unsatisfactory final outcome back to its origins, and Figure 1 below shows the progression of an early idea to a large scale high-tech business, along with stages of finance and net profit.

In the US, all six companies with valuations exceeding €1,000bn were founded in the past 50 years. Comparatively, no European company with a capitalisation of over €100bn has been founded during the same period. Furthermore, between 2008–20, almost 30% of ‘unicorns’ that started in Europe, i.e. start-ups with a turnover greater than $1bn, decided to relocate their HQ abroad. This lacklustre performance does not reflect a lack of ideas; rather, an inability to translate ideas into commercial success at the local level,4 with only one-third of patents registered by European universities being commercially exploited. Some of the issues may be cultural (e.g. different national attitudes to failure, an inevitable aspect of risk-taking) but the chief issue relates to the availability of scale-up capital, as illustrated in Figure 1 below.

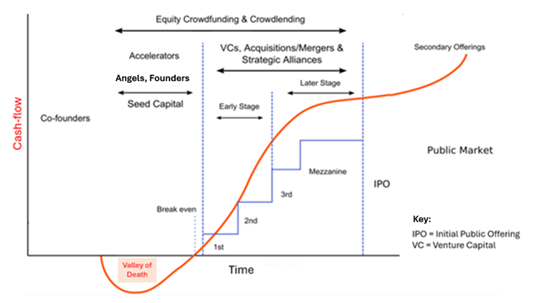

Figure 1 Funding of scale-ups

The figure shows that there is a period of negative cash flow in the early stages (colourfully known as the ‘valley of death’5) that must be met from the founders initially (pre-seed capital), and then by seed capital from angel investors and founders and then, possibly, by accelerators. Even if revenue begins to develop at this stage (as seen by cumulative cash-flow improving to the point of break-even), scale-up cannot occur without major injections of venture capital, otherwise the potential product or service is unlikely to escape the valley of death. The venture capital market in Europe is fragmented and evidence suggests that it struggles to provide the necessary support to start-ups. Consequently, one solution is the deepening of capital markets,6 and an interim step could be giving the European Investment Fund a more active and expanded role in stimulating venture capital markets.7

In addition to private capital, there is public capital, and the EU supports R&D with public capital to the same degree as the US (when measured as a proportion of GDP). However, few funds are allocated at the EU level. Draghi proposed to focus the funds on a smaller number of agreed priorities (three, in total) which are discussed in turn below.

- Artificial intelligence (AI), as an immediate priority. The data and computing capacity necessary to train a foundation-level AI model is typically seen as prohibitive, though the emergence of DeepSeek has, to some extent, challenged this notion. However, within the application layer of the AI value chain, there are many opportunities to build on existing foundation models that may increase productivity in the European industries, while also investing in new skills to exploit the new technologies.

- Focusing R&D on decarbonisation to enhance competitiveness. Although the prime objective of decarbonising is to limit climate change, one of the consequences will be lower cost energy—an imperative given that ‘EU companies face electricity prices that are 2-3 times higher than those in the United States and in China.’8 Draghi’s proposal is to pursue decarbonising in a technology-neutral manner, including renewables, hydrogen, bioenergy, nuclear and carbon capture as appropriate.

- Strengthening security and defence. Given the break-down of the previous global model, there is a need to secure industrial supplies and also provide for adequate defence capability, with the latter addressing the fragmentation of the industrial base. Furthermore, in 2022 almost 80% of total spending on defence went to non-EU suppliers. This report therefore recommends consolidation with the aims of scale advantages, standardisation and inter-operability.

Finally, the Draghi report highlights the sheer scale of the necessary investment to achieve its objectives—namely, €750–800bn additional investment each year. As the GDP of the EU is €17,000bn,9 this represents up to 4.7% of GDP every year, which is more than double the size of the post-WWII Marshall Plan.

The UK’s approach

Almost all of the issues discussed by Draghi are relevant to the UK, with the exception of the comments on venture capital markets, which are typically better-developed and indeed lend to EU companies. There is also a wide range of existing schemes for publicly funded R&D, which is discussed further below. However, the paradox is that the need for action in the UK is possibly even more urgent, as it suffers from a decade of flat productivity.10

To illustrate, on introduction to his report to the European Parliament,11 Draghi noted:

‘We are the most open: our trade-to-GDP ratio exceeds 50%, compared with 37% in China and 27% in the United States. We are the most dependent: we rely on a handful of suppliers for critical raw materials and import over 80% of our digital technology. We have the highest energy prices: EU companies face electricity prices that are 2-3 times higher than those in the United States and in China. We are severely lagging behind in new technologies: only four of the world’s top 50 tech companies are European.’

Yet, in applying those criteria to the UK, the situation is even more critical.

- UK trade-to-GDP ratio was reported at 64% in 2023, according to the World Bank collection of development indicators.12

- The economy is heavily dependent on imports, including digital technology (e.g. the original proposal to source 5G equipment from China, which has since been reversed).

- UK electricity prices are 27% higher than EU prices.13

- There are no UK companies in the top 50 tech companies.

Fortunately, the UK’s plans to correct the situation are in place. There is also a ‘modern industrial strategy’ called Invest 2035 that has identified eight priority sectors: advanced manufacturing, clean energy, creative industries, defence, digital industries, financial services, life sciences, and professional and business services. These are similar to the European priorities but with the addition of service sectors that the UK perceives to be areas of relative strength. The four ‘missions’ of the strategy are driving economic growth, fostering innovation, enhancing global competitiveness and ensuring tangible impact across the UK.

In terms of fulfilment, the mechanisms for making public capital available to growth industries include UK Research and Innovation (UKRI), whose main mission is to support and fund research, innovation, and knowledge transfer. It brings together seven research councils,14 Research England (that co-ordinates universities) and Innovate UK, which focuses specifically on business innovation and provides grants, funding competitions, and advice for innovative businesses in sectors such as AI, robotics, digital technologies, and clean energy. It offers support for start-ups, small to medium enterprises (SMEs), and established businesses to scale their high-tech solutions and bring them to market.

Other support mechanisms from public funds include the following.

- R&D Tax Credits, which can include a direct reduction in corporation tax or a cash rebate for smaller businesses.

- The British Business Bank, which supports access to finance for innovative and high-tech businesses that might find it challenging to secure traditional funding.

- Venture Capital and Angel Investment programmes, such as the Enterprise Investment Scheme (EIS) and the Seed Enterprise Investment Scheme (SEIS) which offer tax reliefs to investors who invest in early-stage high-tech businesses.

- Tech Nation, a government-backed organisation that provides resources, networking, and support for digital and tech companies across the UK. It focuses on scaling tech businesses and fostering innovation.

- National Productivity Investment Fund (NPIF) that supports innovation and the development of high-tech solutions in the digital and tech sectors.

- Regional Growth and Innovation Funds that comprise regional funds across the UK and provide investment to encourage the growth of high-tech businesses in local areas, such as the Northern Powerhouse initiative, funding from Scottish Enterprise, or the Smart Cymru programme.

- Catapult centres, formed by a network of research and innovation centres that focus on different sectors.15 They help businesses collaborate with academia and industry experts to bring high-tech ideas to market, by providing state-of-the-art facilities, expertise, and collaborative networks, accelerating innovation and business growth.

With many different routes to channel investment to the priority sectors, it will be vital to empirically test the effectiveness of each of these mechanisms in achieving the aim of improving competitiveness and growth as part of the ongoing monitoring.

Many of these UK initiatives have their echoes in the EU—for example, the European Institute of Innovation and Technology (EIT) have hubs and communities, and it has even taken the ‘catapult’ name in one recent case.16 However, the creation of the UK’s centres in 2010 was partly modelled on the Fraunhofer Institutes in Germany, following a report by Dr Hermann Hauser.17 We see similar responses in the UK and EU to common issues, but moulded by differences in local conditions.

Despite this impressive array of public funding mechanisms, it will remain the case that most of the capital will originate from the private sector. The emphasis here has been on regulatory and institutional reform, described in the first article in this series,18 and hence not repeated here, except to note that the aims of the UK are similar to those of the EU—namely, to reduce regulatory frictions and to increase the availability of equity funding, using sources such as private savings, and to use public debt for selective growth opportunities.

Conclusion

Whether the funding is coming from public or private sources, there is a need for a massive increase in capital expenditure to boost productivity and competitiveness in the long run. Similar key sectors have been identified in both the UK and the EU, as well as similar sources of capital. It is now imperative to enact the investment programme without delay. Indeed, this is already happening in Germany with the March 2025 ‘whatever it takes’ proposal, to allow for potentially unlimited borrowing for defence spending and the creation of a €500bn 10-year fund to drive infrastructure investments.19 That fund will meet much of the €600bn spending gap that Germany needs to fill to improve its infrastructure.20 The earlier Draghi proposals are now being enacted and funded.

Footnotes

1 Draghi, M. (2024), ‘The future of European competitiveness’, European Commission, p. 5.

2 Oxera (2025), ‘The European growth problem and what to do about it’, Agenda, February

3 Amazon; Apple; Alphabet; Samsung Electronics; Foxconn; Microsoft; Jingdong; Alibaba; AT&T; Meta; T-Mobile; Dell Technologies; Huawei; Sony; Tencent; Hitachi; TSMC (Taiwan Semiconductor Manufacturing Company); LG Electronics; Intel; HP Inc.; Lenovo; Panasonic; Accenture; Nvidia; IBM; Cisco Systems; Oracle; Qualcomm; Ericsson; Xiaomi; Adobe; Broadcom; SAP; Micron Technology; Texas Instruments; NEC Corporation; Fujitsu; Western Digital; ASML Holding; Nokia; VMware; Salesforce; Uber Technologies; Spotify; ServiceNow; Square (Block, Inc.); Shopify; Zoom; Palantir Technologies; Snap Inc.

4 Mack, S. (2024), ‘Europe ventures forward: Getting the scaleup of cleantech right’, 30 October.

5 House of Commons Science and Technology Committee (2019), ‘Bridging the Valley of Death: Improving the Commercialisation of Research’, London.

6 Fratto, C., Gatti, M., Kivernyk, A., Sinnott, E. and van der Wielen, W. (2024), ‘The scale-up gap: Financial market constraints holding back innovative firms in the European Union’, European Investment Bank, June.

7 Arnold, N., Claveres, G. and Frie, J.M. (2024), ‘Stepping up venture capital to finance innovation in Europe’, IMF.

8 ‘Address by Mr. Draghi – Presentation of the report on the Future of European competitiveness – European Parliament – Strasbourg – 17 September 2024’, p. 1.

9 ‘Facts and figures on the European Union’, https://european-union.europa.eu/principles-countries-history/facts-and-figures-european-union_en, accessed 7 March 2025.

10 Bhattacharjee, A., da Silva Gomes, E., Marioni, L., Pabst, A., Smith, R. and Szendrei, T. (2024), ‘Productivity’, National Institute of Economic and Social Research: General Election Briefings, June.

11 ‘Address by Mr. Draghi – Presentation of the report on the Future of European competitiveness – European Parliament – Strasbourg – 17 September 2024’.

12 Trading Economics, ‘United Kingdom – Trade (% Of GDP)’, https://tradingeconomics.com/united-kingdom/trade-percent-of-gdp-wb-data.html, accessed 7 March 2025.

13 Bolton, P. (2025), ‘Gas and electricity prices during the “energy crisis” and beyond’, House of Commons Library, (No. 9714), February.

14 The seven research councils under UKRI are: Arts and Humanities Research Council (AHRC); Biotechnology and Biological Sciences Research Council (BBSRC); Economic and Social Research Council (ESRC); Engineering and Physical Sciences Research Council (EPSRC); Medical Research Council (MRC); Natural Environment Research Council (NERC); and the Science and Technology Facilities Council (STFC).

15 The Catapult centres are Cell and Gene Therapy; Connected Places; Compound Semiconductor Applications; Digital; Energy Systems; High Value Manufacturing; Medicines Discovery; Offshore Renewable Energy; and Satellite Applications.

16 EIT Health, ‘EIT Health Catapult: fast-tracking Europe’s best start-ups‘, https://eithealth.eu/programmes/catapult/, accessed 7 March 2025.

17 Hauser H. (2010), ‘The Current and Future Role of Technology and Innovation Centres in the UK’.

18 Oxera (2025), ‘The European growth problem and what to do about it’, Agenda, February.

19 Financial Times, ‘Germany’s “whatever it takes” spending push to end years of stagnation’, https://www.ft.com/content/ee20978f-bbcd-4616-954c-7749dc5334fd, accessed 7 March 2025.

20 The €600bn estimate was made by the German thinktank IW last year, with a third of the amount spent on decarbonisation. See https://www.iwkoeln.de/en/studies/simon-gerards-iglesias-michael-huether-investment-needs-in-infrastructure-and-for-the-transformation.html, accessed 7 March 2025.

Related

When does a discount become deceptive? An economic framework for the regulation of reference pricing

The use of ‘reference’ pricing—where a previous (or future) ‘was’ price is displayed alongside the current ‘now’ price to indicate a discount for customers—is a common feature across digital and physical markets. In supermarkets, retailers commonly advertise a headline Recommended Retail Price (RRP), or ‘was’ price, alongside the current… Read More

No water, no growth: tackling inefficient business water demand

Water is not typically thought of as a constraint on economic growth in England. Yet that is precisely what it is becoming. Commercial growth and new developments are being turned away because there is insufficient water to serve them. Some water companies are already exercising their powers to refuse… Read More