The strange case of water regulation in Italy

As Professor Alessandro Petretto, teaching Public Economics at the University of Florence, said to me in 1994 when I was researching my thesis paper: ‘there are many initiatives for the reform of Italian public utilities. I do believe that the most interesting, at the moment, are those in energy and telecommunications; the others, related to transport, waste collection and management and water, seem hindered by the relevant roles and powers still attributed to Regions and Municipalities in those fields.’

Professor Petretto proved to be a wise man: at the start of 2000, while the liberalisation processes of energy and telecoms services were being consolidated, Italian institutions were still investigating the reasons for the delays in implementing transport, waste and water reforms. In water, initiatives to overcome the main critical issues were reinforced, first with a reform in 2006, and, subsequently in 2009, by the approval of a new law concerning the reorganisation of the supply chain. This law introduced an obligation either to partially sell 100% publicly owned enterprises or to assign their entrustment contracts through auction procedures.

Before 2012

At the time, water regulation was undertaken on a contractual basis, with each entrustment contract defining the risk-sharing clauses among the parties, and tariffs established on the basis of projected variables: capital expenditure (CAPEX), operating expenditure (OPEX) and water consumption. There was also an obligation to hold an investigation every three years, to verify whether any differences in projected values, including tariff and outturn values, were due to end-users (e.g. reduced consumption) or operators (e.g. cost inefficiency). The implementation of this obligation was highly unsatisfactory, generating a loss of transparency and damaging the reputation of the parties. As a result, there were many litigation cases between consumers (unwilling to pay for investments planned but not yet realised) and operators (asking for full recovery of actual costs). The sector outlook appeared disordered and uncomfortable.

Furthermore, a referendum result in 2011 established that a fair rate of return should not be included in the water tariff calculations, and that the obligation either to partially sell 100% publicly owned companies or to assign their entrustment contracts through auction procedures was to be abolished.1 Uncertainty over the future of the sector increased. Decision-making processes, among both public institutions and private operators, suggested a common dominant strategy: inertia.

A few months later, the government proposed assigning the water tariff regulation, contract design, monitoring and regulatory enforcement to an independent regulator, the Italian Electricity and Gas Authority. Parliament approved this and changed the institutional framework for water services. Two years later the regulator’s name was changed accordingly to the Independent Regulatory Authority for Electricity, Gas and Water (AEEGSI). The new institutional framework appeared to be in line with OECD recommendations on regulation2 and promoted international cooperation in the field of water regulation, leading to the foundation in 2014 of WAREG (the Network of European Water Sector Regulators).3

In terms of tariff regulation, the responsibilities assigned to AEEGSI were twofold:

- ex ante, to define cost reimbursement rules and tariff calculation mechanisms;

- ex post, to approve the tariff proposals set out at 68 decentralised levels (‘EGAs’) for each of the 150 industrial operators4 and 2,500 municipalities (which are predominantly still in charge of the sewerage systems and are located in the south of Italy).

In early 2012 AEEGSI’s regulatory activity began by focusing on setting: i) tariffs; ii) compulsory standards for quality of service with incentives, penalties and refunds; iii) conditions for service supply and contracts; and vi) rules for accounting unbundling.

The key developments since then are discussed below.5

First regulatory period, 2012–15

The framework

In 2012 AEEGSI published several consultation papers on the tariff regulation reform that it was proposing. By the end of that year Decision 5856 was adopted, introducing a significant change: an ex ante method of tariff calculation (i.e. using expected cost) was turned into an ex post method (in which the relevant inputs to the calculation were measured). To promote efficiency, an overall cap on revenues was introduced; OPEX based on controllable outturn OPEX in a base year was rolled forward; and standardised parameters for the ‘reimbursement’ of fiscal and financing costs to operators were established on a notional basis. At the same time, AEEGSI concluded a procedure to reimburse consumers with the difference between the allowed return on capital included in the tariff (charged by water service operators under pre-referendum regulation) and the notional fiscal and financing costs. Overall, this increased regulatory transparency and the sector’s accountability.

In 2013 AEEGSI began consulting on identifying the long-term objectives of regulation, and examined a new tariff mechanism within which all the relevant features of the Italian water sector would be considered. Decision 643 (the ‘MTI’) was adopted at the end of the year, centred on the ‘Regulatory Matrix’.7 This allowed for regulation to vary depending on the initial operating circumstances of each operator. The overall framework was designed to introduce a set of innovative and asymmetric rules, which provided incentives to invest. In order to identify the specific rules applicable to tariff calculation, the MTI considered two key features:

- the ratio between the planned investment expenditure and the regulatory asset base (RAB)—if this ratio was above a certain threshold, it would be possible to apply rules to achieve higher cash flows;

- the expansion of activities to be managed by the operator—if new activities have to be managed, their costs have to be recovered and, therefore, included in the allowed revenues.

Outcomes of the first period

AEEGSI has paved the way to a clear, stable and coherent regulatory framework that takes account of the various characteristics of the water sector in Italy. The tariff-setting methodology and regulatory action for the years 2014–15 have proved to be effective:

- tariff changes approved by AEEGSI for 2014–15 apply to 1,970 operators, affecting around 53m Italian citizens. The average increase in charges on the previous year was just over 4.3% in 2014 and 4.6% in 2015;8

- for 135 industrial operators (serving 43m customers), AEEGSI approved tariff proposals consistent with planned investments, amounting to approximately €5.6bn for the four-year period from 2014 to 2017;

- investments (net of public contributions) for the years 2014 and 2015 show particularly strong growth, with a 55% increase recorded in 2015 compared with 2012.

The largest part of the investments has been aimed at dealing with the infrastructure gap in sewerage and sewage-treatment activities on the basis of the priorities defined by the individual EGAs (in agreement with the relevant operator). The overall amount of investment appears to be both an encouraging result when compared with the previous period, and at the same time an unsatisfactory one when compared with international benchmarks (€33 per capita per annum seems insufficient for investment in water distribution, sewerage networks and treatment plants).

One of the main limitations to emerge for the financing of infrastructure relates to the low value of the RAB. There may be many reasons underpinning this, but one can be stated with certainty: a long period of relying solely on public funding of water infrastructure has led to asset depletion and has left operators with a very limited asset base.

Second regulatory period, 2016–19

In December 2015, AEEGSI approved the regulatory package for the new regulatory period. This comprises three elements:

- a new method for defining cost reimbursement rules and tariff calculation mechanisms (‘MTI-2’);

- contractual quality (i.e. quality of customer-facing services such as complaint-handling, call response, connection time, etc.), providing for a gradual harmonisation, throughout the country, of delivery for end-users;

- standard agreement regulation, approving a common framework for the allocation of legal obligations among EGAs and water service operators.

This new and comprehensive regulatory package represents a coherent and broad legal framework.

Cost reimbursement and tariffs

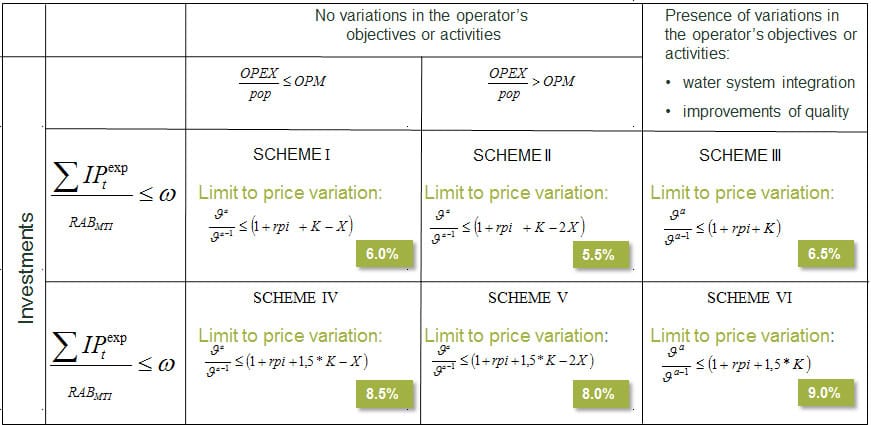

Under MTI-2,9 as under the MTI, the selection of applicable cost-reimbursement rules depends on the specific circumstances of the operators, which place the operators in one of six Schemes in the new Regulatory Matrix for the period 2016–19.10 The Scheme is determined by the EGAs according to two factors:

- the ratio between the investments planned (IP) for the period 2016–19 and the regulatory value of the existing infrastructure (RAB): Schemes I, II and III are characterised by lower investment needs going forward; and Schemes IV, V and VI are suitable for relevant investments, identified according to operator’s objectives;

- OPEX relating to the operator’s specific objectives, where: Schemes I and IV (for more efficient operators, with per-capita OPEX below the national average value, OPM) and Schemes II and V (for operators with per-capita OPEX greater than OPM) are characterised by unchanged specific objectives and scope of activities; and Schemes III and VI are applicable in the event of a structural change in the activities, in terms of served area or scope of supplied services, leading to additional costs being incurred by the operator. The reason behind these schemes is the new legislation that requires existing operators to merge such that, for each EGA’s area, there will be one operator providing water services. The Regulatory Matrix considers this obligation, providing for more favourable rules for merging parties.

On the basis of the identified scheme and relative cost-reimbursement rules, it is possible to determine the tariff multiplier, ϑ. This is calculated as the ratio of the allowed amount of cost recovery expected in one year to the revenue corresponding to the tariff applied in the base year. The cap on revenues applies to the increase of the tariff multiplier, defined on the basis of the estimated retail price index variation, a K factor—taking into account the investment needs and the guarantee of standardised financial viability of operators—and an X factor, a past efficiency-sharing factor. Every single tariff charged to end-users has to grow in line with, or less than, the tariff multiplier (the maximum growth for each scheme is shown in the green boxes in Figure 1).

Figure 1 Tariff-setting in the second regulatory period

Source: AEEGSI (2015), ‘Approvazione del metodo tariffario idrico per il secondo periodo regolatorio MTI-2’, Delibera 664/2015/R/IDR.

Contractual quality

Incentives for improving the quality of the service provided to users will not come from tariff rules alone, but also from compliance with the regulation concerning the contractual quality of the water service. The latter aims to strengthen the protection of end-users and reduce local differences by introducing minimum quality standards.11 This decision recognises the additional costs arising from improvements in quality beyond the minimum standards, and introduces an incentive mechanism based on compensation, penalties and rewards.

In this area, the role of the EGAs is fundamental, as they possess greater information regarding the specific context, thus allowing them to identify the needs of local communities and aim for a quality of service higher than the minimum national standard. They can achieve this through the incentive mechanism, with rewards for operators paid for by users benefiting from higher standards.

Standard agreement

AEEGSI has also introduced a standard agreement to regulate contractual relations between local authorities and operators.12 It is an important instrument in defining the contractual framework at a local level and ensuring certainty and affordability of the general regulatory framework. In particular, the standard agreement sets: i) the maximum duration of public concessions and conditions for their possible extension; ii) instruments to ensure operators’ financial viability; iii) terms and procedures for asset payment at the end of the concession (terminal value); and iv) risk-sharing among operators and local governments, which is diversified according to the operators’ selected organisational model.13

Next steps

AEEGSI has recently approved the regulation of accounting unbundling in the water sector and, at the same time, has delivered a toolkit for tariff calculation and planning. Moreover, a broad consultation on metering has been put in place, and an even broader one is planned on technical aspects of quality of service (e.g. interruptions and resilience). Thus the key building blocks for the development of a long-lasting regulatory framework have been laid in a relatively short period of time.

However, there is ongoing controversy relating to the regulation of the cost of infrastructure. The new regulatory approach to financing and fiscal costs was not accepted by those in favour of the referendum or industrial operators, and, in 2013, this led to a legal dispute which continues to this day. The final decision is expected by the end of 2016 (it was originally planned for September 2015). As is always the case, AEEGSI will abide by the court’s decision. However, it will continue to promote regulatory initiatives for a less strange and a more stable, predictable and accountable water sector.

Lorenzo Bardelli

Download

Related

No water, no growth: tackling inefficient business water demand

Water is not typically thought of as a constraint on economic growth in England. Yet that is precisely what it is becoming. Commercial growth and new developments are being turned away because there is insufficient water to serve them. Some water companies are already exercising their powers to refuse… Read More

The energy trilemma in focus: the price of dependence

Europe’s approach to energy policy has been in transition since the 2022 energy crisis laid bare the continent’s dependence on imported fossil fuels. More recently, the outbreak of war in the Middle East and the subsequent disruption to global oil and gas markets have caused further challenges. This article… Read More