Regulating oligopolies in telecoms: a solution in search of a problem?

Telecommunications markets across Europe have recently gone through significant change. The deployment of next-generation access (NGA) networks (i.e. with speeds in excess of 30Mbps), competition from cable networks, technological convergence, and a wave of M&A activity in the sector have contributed to the emergence of ‘oligopolistic’ markets: a small number of competitors using their own infrastructure to offer bundles of fixed, TV and mobile services.

In this context, the question has been raised as to whether the existing EU regulatory framework, which is based on the SMP (significant market power) framework (which traditionally covers single-firm dominance and joint dominance), is suited to dealing with oligopolies, or whether new regulatory tools are required.

This article summarises Oxera’s contribution to this debate, based on a discussion paper commissioned by Liberty Global on whether and how to regulate oligopolies in electronic communications markets.1

This debate is of critical importance for the telecoms industry. As the Commission has observed, reaching Europe’s connectivity objectives is likely to require €500bn of investment, most of it from the private sector, and under current investment trends there is an estimated €155bn shortfall.2 A stable and predictable regulatory environment will help to provide investors with the confidence needed to invest these amounts.

The calls for new regulatory tools

Back in 2015, BEREC suggested that there might be an oligopoly blind spot at the heart of the telecoms regulatory framework—in particular, regarding what BEREC has described as ‘tight’ oligopolies: market structures that cause non-effective market outcomes without explicit collaboration, tacit collusion or dominance.3

To address this perceived problem, BEREC has made a recommendation to the Commission to incorporate a test for UMP in the new European Electronic Communications Code and in the revised SMP Guidelines. BEREC defines the concept of UMP as a situation where firms are not coordinating their behaviour—and therefore do not have joint SMP—and nor do they possess single SMP, but they have the unilateral incentives and the ability to behave in ways that lead to ineffective competition and poor consumer outcomes.4

In addition to this proposal, which has been endorsed by the European Parliament’s Committee on Industry, Research and Energy, there are other policy initiatives seeking to introduce greater regulatory oversight in oligopolistic markets. Most notably, these include requests by some member states in the European Council to extend the scope of symmetric access obligations beyond the first concentration point, irrespective of a finding of SMP.

In addition, the Commission’s public consultation on updating the guidelines on market analysis and SMP is generating debate over whether the standard of proof to find joint SMP is too high, and how further guidance could assist national regulators in proving its existence.5

In the discussion paper, Oxera examines whether the calls for new regulatory tools outlined above are justified in light of the Commission’s policy objectives.

From monopolies to infrastructure competition

Over the past 20 years many European telecoms markets have evolved from monopolies to markets with significant infrastructure competition, which is delivering considerable consumer benefits.

The EU regulatory framework of 1999, and its amendment in 2002, was designed to be a transitional arrangement aimed at kick-starting competition in the market, with increasing reliance on general competition rules as competition became more effective.6 To a certain extent, regulators have lived up to this promise. In the regulatory framework, the number of relevant markets that are susceptible to ex ante regulation fell from 18 in 2002 to 7 in 2007 and 4 in 2014, all of them wholesale markets. Retail price regulation has been withdrawn in most of Europe, with regulation focusing instead on upstream bottlenecks.

The original rationale for the SMP framework for providing access to bottlenecks at different points in the incumbents’ networks was to allow access operators to climb the ‘ladder of investment’, starting as resellers and building enough scale to gradually roll out infrastructure of their own, and one day make the final jump to building their own networks. While successful at creating an access market, the framework has not quite delivered on the ultimate promise of infrastructure-based competition.7

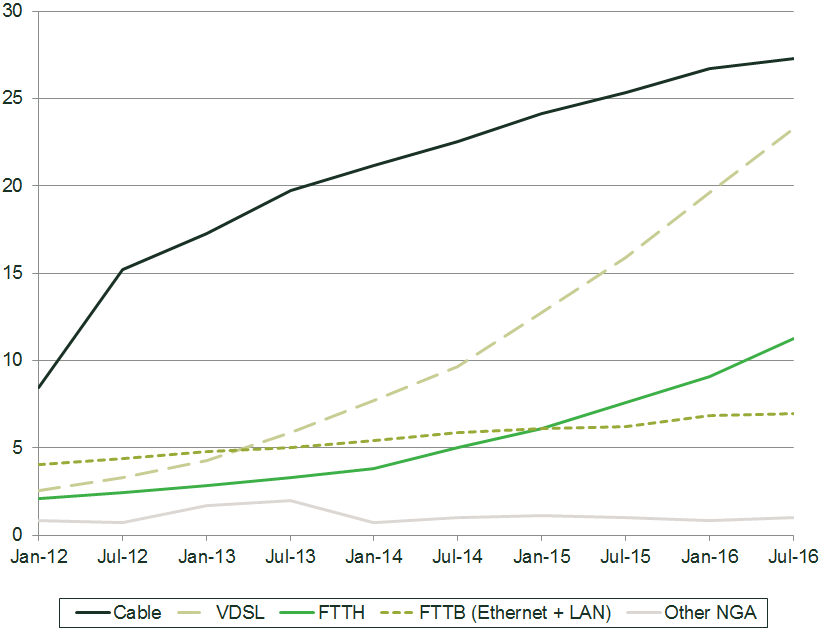

Nevertheless, the trend towards convergence and consolidation is reshaping the landscape. Technological innovation and convergence, and the continued growth in, and consolidation of, cable networks, are contributing to increased facilities-based competition in the broadband market. Overall, the market share of incumbents in the EU has decreased by 10 percentage points since 2006.8 Cable and alternative fibre networks increasingly compete with legacy copper networks, and account for an increasing proportion of NGA subscriptions, as shown in Figure 1.

Figure 1 NGA penetration in the EU (≥30Mbps) by technology (millions of subscriptions)

Source: Communications Committee, cited by European Commission (2017), ‘Connectivity Broadband market developments in the EU – Europe’s Digital Progress Report 2017’, 27 April, slide 20.

Furthermore, all across Europe, new networks with very high capacity are being rolled out, relying on a variety of funding mechanisms and technologies. These include co-investments using the networks of other utilities, such as energy distribution. By the time the European Electronic Communications Code has entered into force and is transposed into national laws, the deployment of 5G mobile networks will be in full swing, capable of delivering speeds comparable to those of fixed broadband networks. Hence, competition between different network infrastructures is set to intensify even further.

Looking to the future, the demand for bandwidth is expected to increase nearly threefold over the coming five years,9 which is expected to drive competition among the different fixed and mobile infrastructure operators to invest in new technologies.

These trends are consistent with a large body of empirical evidence that demonstrates that infrastructure competition is the main driver of investment in NGA networks, increasing the penetration of high-speed broadband services, and leading to improvements in network coverage and speed, as well as lower prices for consumers.

Against this background, rather than seeing it as a cause for concern, regulators should embrace infrastructure competition and consider whether, in some markets, the time for stepping back from ex ante regulation and relying on competition law to address oligopoly concerns may finally have come. After all, this is precisely what the EU electronic communications framework of 1999 and 2002 envisaged.

The existing regulatory toolkit continues to be fit for purpose

In specific market situations defined by the existing SMP framework, competition may not be effective and regulation may be required. However, the rise of oligopolistic market structures in itself should not be a cause for concern.

Economic theory and empirical evidence show that oligopolies come in many flavours. Structural market features on their own cannot provide strong evidence of whether competition between oligopolists will be effective. Markets with just two operators competing with differentiated but substitutable products and different cost structures, and facing significant competitive constraints from external forces such as online platforms and over-the-top services, can produce significantly more competitive outcomes than markets with many operators but more homogeneous products, cost structures and technologies.

The key is whether consumers are receiving the benefits of competition through high-quality networks, innovative products and services, and competitive prices, given the underlying cost of the infrastructure. Where this is not the case, this can be indicative of ineffective competition—i.e. markets with limited churn, stable demand, few product and service innovations, limited investment in new technologies, and prices that are considerably in excess of the cost of production. In these circumstances, the conditions for finding tacit collusion under the ‘Airtours criteria’ (transparency around a focal point of coordination; effective punishment mechanisms; and no external destabilising forces), and hence joint SMP, can be applied as in any other sector.

Those seeking to add new tools to the regulatory framework claim that the relative paucity of cases where regulators have found joint SMP (and that have survived scrutiny by the Commission and national courts) is caused by a lack of clarity on the standards and evidential thresholds that regulators must meet.10

According to Oxera’s analysis, however, the limited number of joint SMP findings is neither surprising nor a cause for concern. It is not surprising because telecoms markets typically do not display the characteristics of markets that are prone to tacit collusion. Furthermore, there is no empirical evidence that oligopolistic market structures have been detrimental to consumer welfare, absent coordination. In fact, quite the opposite, as we have shown above.

It is therefore unclear what market failure the proposed UMP test would seek to correct. UMP would require an arbitrary demarcation of criteria and market outcomes below which markets are allegedly not working effectively, but where this is not the result of single-firm SMP or tacit collusion. UMP would occur when firms provide sufficiently close competitive constraints to each other to be included in the same relevant market, but close enough to prevent each other from exercising market power. This interpretation means that, in many cases, UMP may simply be a milder version of SMP, providing regulators with considerable freedom for intervention.

The risk of over-regulation is also illustrated by BEREC’s reference to the ‘significant impediment to effective competition’ (SIEC) test as a justification for the UMP concept. BEREC makes the analogy that the SIEC test closed a perceived enforcement gap in merger control (the so-called unilateral effects gap), thereby allowing regulators to block or address harm caused by transactions involving non-dominant companies.

However, whereas the SIEC test is used to assess changes in the degree of competition resulting from specific changes in market structure (i.e. mergers), and hence deals with relative levels of competition, the UMP test would be used to assess the absolute level of competition for a given market structure (i.e. with no specific change in the market structure). Therefore, while superficially similar, the SIEC and unilateral effects tests in mergers do not provide a guide or blueprint for the UMP test as proposed by BEREC.

The proposal to extend symmetric access obligations on infrastructure competitors beyond the first concentration point is also problematic from an economics perspective. Aside from the fact that this proposal is predicated on the factually inaccurate premise that passive and active network elements are essential facilities that cannot be easily duplicated, the proposal would bypass the market review process, allowing regulators to impose access obligations on any network owner regardless of their position in the market. Such a remedy is likely to have a negative effect on investment incentives.

Concluding remarks

The key findings of the Oxera discussion paper for Liberty Global are summarised in the box.

Key findings of Oxera’s discussion paper

- Regulators should not be concerned by the rise of oligopolistic market structures, since these structures are driven primarily by desirable infrastructure-based competition—investment by infrastructure providers has increased competition and eroded the market power held by incumbents. Market outcomes for consumers in terms of prices and quality (for example, in broadband speeds) have improved significantly. With increased competition from cable networks, a growing number of fibre investment projects, and the advent of superfast mobile broadband from 4G and 5G mobile networks, the time seems right for regulators to step back and rely on competition law to address any oligopoly concerns (other than tacit collusion), as originally envisaged by the 1999 and 2002 EU regulatory frameworks.

- Expanding the regulatory toolkit to include unilateral market power (UMP), or expanding symmetric access obligations, will increase the risk of over-regulation, introduce uncertainty, and diminish investment incentives—the proposals from the Body of European Regulators for Electronic Communications (BEREC) and some member states for UMP and the expansion of symmetrical access do not have a solid grounding in economic theory. UMP is also very different from the concept of unilateral effects in merger control. Finding objective criteria and an unambiguous threshold below which markets can be characterised as ineffectively competitive in the absence of SMP is fraught with theoretical and practical problems. Implementing such proposals would provide significant discretion for regulators to intervene in markets, reducing regulatory certainty and creating a more fragmented regulatory landscape across Europe. This seems to be the opposite of what is required to meet Europe’s connectivity objectives.

- The criteria for establishing joint SMP are sufficiently understood in case law and economic theory—an ‘enforcement gap’, if any, is small and does not need to be addressed by additional ex ante regulation such as UMP or expanded symmetrical access. Few competitive problems are not covered by the current SMP and competition rules, and any enforcement gap is small (and the relevant policy question is in any event not whether such a gap exists, but what its optimal size is and whether the benefits of addressing it are outweighed by the costs). The apparent paucity of cases involving joint SMP is not due to a lack of understanding about how to implement the test. Rather, it reflects the fact that, in many telecoms markets where there is no longer a single incumbent with SMP, competition tends to be effective and to produce good consumer outcomes. Wholesale access still has a role to play in creating the conditions for effective competition where single-firm dominance continues to exist. The UMP proposal for dealing with oligopolistic market structures lacks justification.

Source: Oxera (2017), ‘Regulating oligopolies in electronic communications markets’, discussion paper prepared for Liberty Global, September.

The relevant questions for the policy debate on regulating oligopolies are: whether an enforcement gap exists; what its optimal size is; whether it should be addressed by additional ex ante regulation; and whether the benefits of additional regulation are outweighed by its costs.

In any unregulated market that is not perfectly competitive, there could be said to be an enforcement gap. However, this provides little guidance for meaningful debate on the optimal degree of regulatory intervention.

In this context, it is important to note that a large range of potential competition problems in electronic communications markets can already be dealt with under existing regulation and antitrust rules:

- the existing SMP standard in telecoms regulation covers both single-firm dominance and joint dominance based on tacit collusion;

- Articles 101 and 102 of the Treaty on the Functioning of the European Union (TFEU) cover a variety of anticompetitive behaviours, including various forms of exclusion and discrimination;

- merger control deals explicitly with potential increases in concentration, and the risk of coordination and unilateral effects as a result of mergers.

In addition, regulators can influence competitive dynamics by using consumer protection powers, as well as by exercising regulatory discretion—for example, in relation to spectrum auction rules—with a view to increasing competition in the market. In all, Oxera considers any potential enforcement gap to be small.

The Commission’s connectivity targets are ambitious. By 2025, it envisages reaching 100% coverage of networks delivering over 100Mbps, with the capability of being upgraded to 1Gbps. A stable and predictable regulatory environment will help to achieve this.

Our analysis shows that the calls for enhanced regulatory tools—UMP, expanding symmetric access, and the potential lowering of the standard of proof for finding joint dominance—are likely to achieve the opposite. They risk introducing legal and economic uncertainty that will reduce investor confidence at a time when it is needed to boost investment in fibre broadband and deliver on Europe’s ambitions for a gigabit society.

This article is based on Oxera (2017), ‘Regulating oligopolies in electronic communications markets’, discussion paper prepared for Liberty Global, September.

1 Oxera (2017), ‘Regulating oligopolies in electronic communications markets’, discussion paper prepared for Liberty Global, September.

2 European Commission (2016), ‘State of the Union 2016: Commission paves the way for more and better internet connectivity for all citizens and businesses’, press release, accessed 19 July 2017.

3 BEREC (2015), ‘Report on oligopoly analysis and regulation’, BoR (15) 74, June, p. 48.

4 BEREC (2017), ‘BEREC views on non-competitive oligopolies in the Electronic Communications Code’, BoR (17) 84.

5 European Commission (2017), ‘Public Consultation on the Review of the Significant Market Power (SMP) Guidelines’, 27 March, accessed 19 July 2017.

6 European Commission (1999), ‘A new framework for electronic communications services’, COM(1999) 539 final, 10 November, accessed 19 July 2017. European Commission (2002), ‘Directive 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communications networks and services (Framework Directive)’, 7 March, accessed 14 September 2017.

7 See, for example, Briglauer, W., Cambini, C. and Grajek, M. (2015), ‘Why is Europe lagging on next generation access networks?’, Bruegel Policy Contribution, 14, September.

8 European Commission (2017), ‘Connectivity Broadband market developments in the EU Europe’s Digital Progress Report 2017’, slide 21.

9 See Cisco (2017), ‘Cisco Visual Networking Index: Forecast and Methodology, 2016–2021’, 6 June.

10 See, for example, BEREC (2017), ‘BEREC response to the public consultation from the EC on the update of the SMP Guidelines’, BoR (17) 115, p. 10.

Download

Related

No water, no growth: tackling inefficient business water demand

Water is not typically thought of as a constraint on economic growth in England. Yet that is precisely what it is becoming. Commercial growth and new developments are being turned away because there is insufficient water to serve them. Some water companies are already exercising their powers to refuse… Read More

The energy trilemma in focus: the price of dependence

Europe’s approach to energy policy has been in transition since the 2022 energy crisis laid bare the continent’s dependence on imported fossil fuels. More recently, the outbreak of war in the Middle East and the subsequent disruption to global oil and gas markets have caused further challenges. This article… Read More